Convertible debt

Convertible debt (also called convertible notes) is a form of financing that is often used by high-growth early-stage companies. It starts off as a loan (debt), but the lender and the company have options to convert the debt to equity under certain predetermined terms called “conversion privileges” as specified in the deal’s term sheet. Under such an agreement, the lender generally does not place a valuation on the borrowing company, meaning the current or future value of the company might not be taken into account when the loan is being made. However, in many circumstances, a valuation cap (ceiling) is included in the terms. The lender may add other specific clauses to the note that they would require when and if they become a shareholder.

The agreement sometimes includes a “callable option” which allows the borrower to force conversion when the value of its shares reaches a certain threshold or a minimum financing threshold is reached while the note is outstanding (typically for two or three years).

This type of financing is typically provided by a venture capital firm, angel investor or debt lender.

Lenders or would be investors like convertible debt because it can provide them with interest payments for the duration of the note, discounts typically ranging from 10% to 20% on the ultimate conversion value, and priority ranking over the preferred shares or common shares as outlined in the term sheet until they decide to convert the outstanding debt into equity.

Advantages of convertible debt

Companies typically take on convertible debt when they believe their shares will increase in value. This allows them to reduce equity dilution (giving up too much ownership). For example, if a business wants to raise $1 million and its shares might be worth $20, it would have to sell 50,000 shares to reach its funding target. With convertible debt, it can defer conversion until shares are potentially worth $30 each and issue only 33,333 shares instead, paying interest on the debt before that point. This assumes there is a valuation cap that is approximately 50% above the current value and the funding is above that valuation.

Convertible debt can be easier to issue than an equity investment because nothing needs to be changed in the company’s shareholder’s agreement. Unless already a shareholder in the company, the lender is not party to the shareholders’ agreement until conversion of the debt. This makes it faster to close, and the fees involved can be significantly lower because there is less work involved for lawyers and other professionals.

Convertible notes are especially attractive for early-stage companies which may not have an extensive credit history or a successful track record raising capital. For these companies, this type of financing is often easier to obtain and remains faster and cheaper than traditional equity financing.

This type of funding can also be used as a form of bridge financing, which could be appealing to more mature companies under certain circumstances, especially when the company does not want to set a valuation.

There can be a number of variations within a convertible debt deal. In some cases the debt will convert into common shares, while in other cases it may convert into preferred shares. While convertible debt always has an option to convert to equity, the specific timing and conditions, as well as the value of the equity awarded in exchange for the debt, does vary from one deal to the next. All of this would be outlined in the term sheet.

A model convertible note agreement can be found on the CVCA website.

One caveat related to convertible notes is that if future equity rounds fail to materialize, the debt remains outstanding until maturity. This is a liability for the company which will eventually be redeemed. It is important for both parties to consider how that redemption could be structured when entering into the agreement. These considerations will help ensure the company continues to operate normally once repayment has been completed.

Convertible debt versus debt and equity

| Pros of convertible debt | Cons of convertible debt | |

|---|---|---|

| Versus equity |

|

|

| Versus debt |

|

|

Example of convertible debt

The following example shows how convertible debt could be set up. ABC Company raises $1,000,000 in convertible debt financing from an investor with the following conversion privileges and a callable option:

- Conversion privileges—The loan can be converted into 20,000 common shares in ABC Company at $50 per share within 3 years. Until that point, the lenders will be paid monthly, at an interest rate of 4%.

- Callable option—ABC Company can force the conversion of its convertible debt any time after the end of the first year and when its common shares are valued at 120% of the conversion price, typically for 25 consecutive days or more for a public company or, for private companies, if the borrower raises a certain amount ($2 million for example).

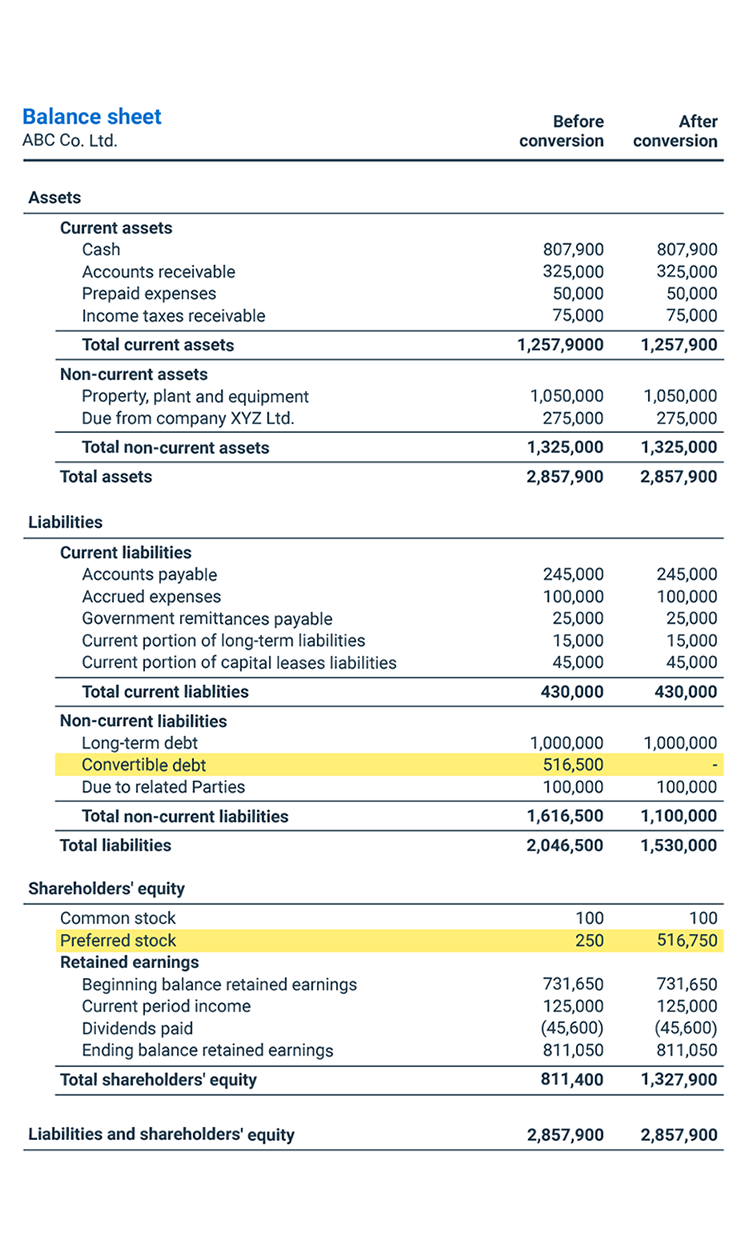

How does convertible debt appear in a balance sheet?

When it comes to asset payout order (the order in which a company’s liabilities are paid off in the event of a sale or liquidation) debt always ranks ahead of equity, meaning the debtholders are first in line to be paid if ever the company is sold or has to cease operations. However, as a security, convertible debt can be viewed as either debt or equity, and so it is ranked just after traditional bank debt but before preferred and then common equity in the payout order. Bank debt would typically rank ahead to the convertible debt, which in turn ranks ahead of the existing investor’s preferred shares.

What this means for a company’s balance sheet is that these securities will most often be listed as convertible debt, a separate category from bank debt or equity.

Convertible debt may be perceived differently by various actors within the financial community. For example, a traditional bank is likely to look at subordinated convertible debt as equity. On the other hand, for a general preferred shareholder convertible debt is looked at like more debt because it ranks ahead of their investments in the payout order. It depends on who’s looking at the security, but for traditional banks, it is treated as equity.

The sample balance sheet below illustrates how a convertible debt conversion can affect a balance sheet. The convertible debt that was listed as a non-current liability before the conversion now gets get treated as shareholder’s equity.

Valuation cap on convertible debt

Lenders/investors will likely ask to include a valuation cap on a convertible note, which can provide them with more certainty on the ultimate investment in the company. This acts as a limit on the value at which the debt can be converted. For example, a company currently worth $20 million taking out a $5 million convertible debt loan may be asked to cap the conversion value at $40 million.

Let’s say that company is then able to grow and eventually raises a series B round at a valuation of $50 million. The lender will then have more favourable terms when the debt converts. Not only will its debt become equity, but the investor could also receive that equity at a 20% discount to the valuation of the round ($40 million vs. $50 million). This compares to an uncapped note which typically is favored by the borrowing company because it means less dilution of its equity at the next round of fundraising.

Discount rate on convertible debt conversion

Term sheets for convertible debt usually also include a discount rate upon conversion, which is another way for early-stage lenders to get better terms in return for their early investment.

As the name suggests, the discount rate allows the lender/investor of the convertible debt to acquire shares at a reduced price versus investors in the next round of financing once the round has closed. As an example, a 10% discount rate would mean obtaining shares valued at $50 million in a series B, for the price of those with a total value of only $45 million. Conversion discounts are usually between 10% and 20%.

Difference between convertible debt and SAFE

Convertible debt must not be confused with simple agreement for future equity (SAFE) notes, which are an alternative form of financing used by early-stage companies.

SAFEs provide investors the opportunity to obtain equity in the company when certain milestones are reached, including raising a round of funding, sale or merger of the business, or other transactions.

Although these resemble convertible debt in many ways, SAFE notes have two important distinctions:

- SAFE notes are not debt obligations and there is no interest obligation with SAFE notes.

- SAFE notes do not have a fixed duration and remain in effect until conversion

Financing toolkit for tech companies

Tech companies have a unique growth trajectory. Use these tailored tools to map business growth and attract new investors.