Canadian Small Business Health Index

The Canadian Small Business Health Index combines survey data collected by BDC, Equifax credit bureau data and macroeconomic data from Statistics Canada and the Bank of Canada. The index complements existing indices and provides a novel perspective on Canadian business health. The index can inform business decisions about strategy and investment.

The index groups four main components of business health:

- Credit performance

- Business growth projections

- Business sentiment

- Business environment

Results by region

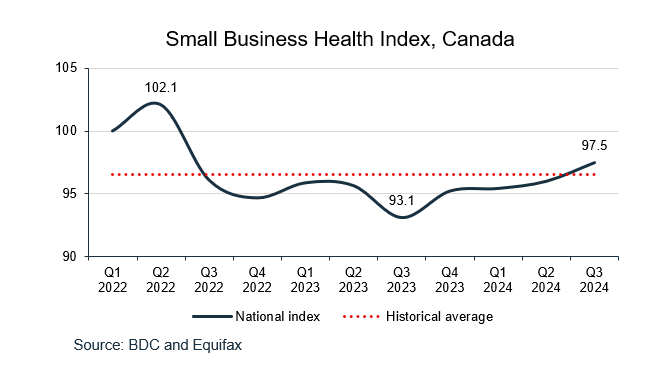

Canada: Slow and steady improvement

Small Business Health Index, Q3 2024

97.5

Year-over-year difference

+4.7%

Difference over the previous quarter

+1.5%

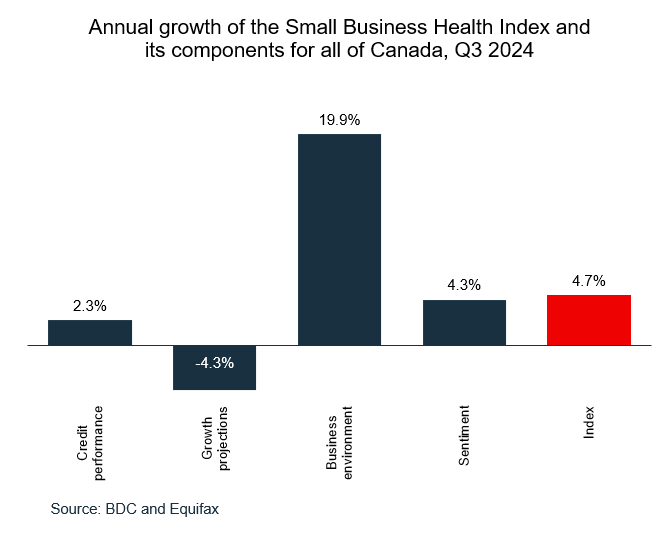

After a sharp decline brought by increasing interest rates, the national index has slowly but steadily improved since the end of 2023. In Q3 2024, it stood at 97.5, a 4.7% increase from last year and a 1.5% increase over the previous quarter.

Improvement of the business environment was the largest contributor to this increase as the economy is starting to show signs of recovery. The inflation rate has returned to the Bank of Canada’s 2% target and the central bank started cutting its policy rate in June 2024. As a result, business sentiment is improving, with SMEs expecting a better economic outlook and access to credit is easing. However, sluggish sales and lower investment plans are still hindering SMEs, which is having a negative effect on the growth projections component. The credit performance of SMEs still hasn’t fully recovered from the impact of high interest rates, even though it is slowly trending in a positive direction.

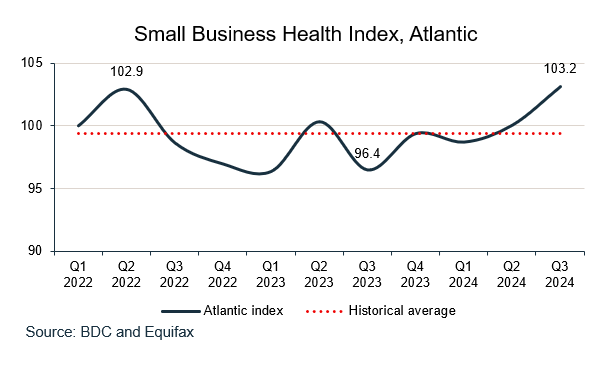

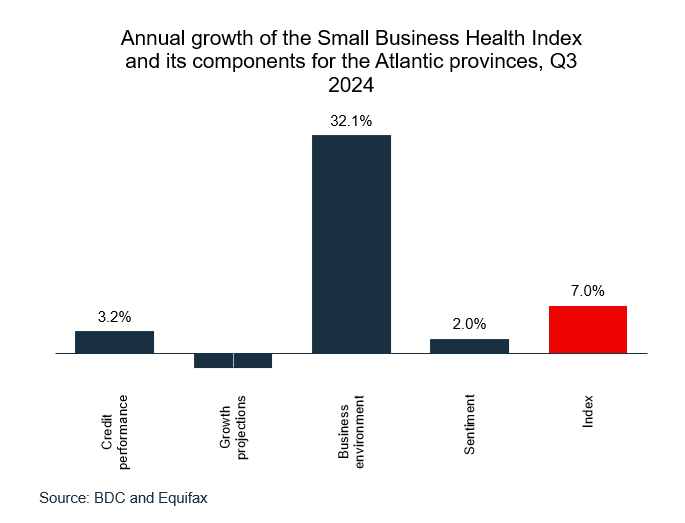

Atlantic: Outperforming the rest of Canada

The Atlantic region outperformed the national index in Q3 2024. It stood at 103.2, posting a 7.0% increase over the same period last year and a rise of 3.1% over the previous quarter. The credit performance of businesses in the region improved while early delinquency rates decreased. There was also stronger employment and wage growth in these provinces, contributing to the strong rise of the business environment component. This also seemed to impact business sentiment, as SMEs had a more optimistic economic outlook.

Strength in housing construction, propelled by the important influx of immigrants to the region and the advancement of multiple major projects, has also contributed to improving the business environment.

Growth projections were lower than last year, even though business openings have increased and existing businesses are expressing greater investment intentions. Cautious household spending is dragging down the outlook for sales growth.

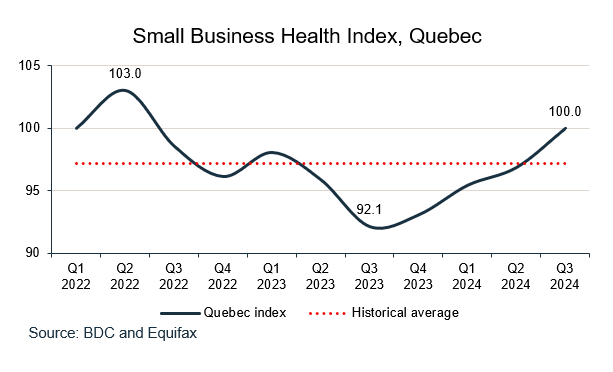

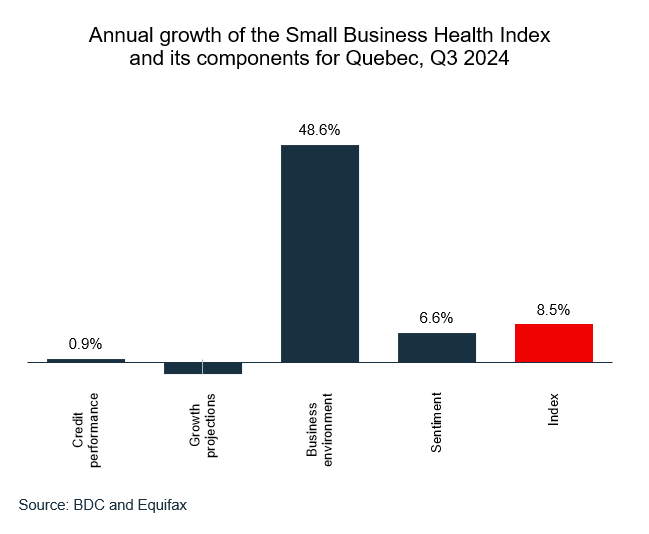

Quebec: Bouncing back from a tough year

Business health in Quebec showed strong increase in Q3 2024 following a stagnant GDP in 2023. Overall, the index stood at 100.0, an 8.5% increase compared to a year ago and a 3.2% increase against the previous quarter.

The business environment component is driving the upward trend on the back of rising wages and a faster return to the Bank of Canada’s inflation target.

Businesses in Quebec are improving on all aspects of sentiment and are expressing stronger investment intentions. However, credit inquiries and new industrial credit account openings fell in the last year, which is dragging down growth projections. This component was only slightly offset by a 16% increase in business openings.

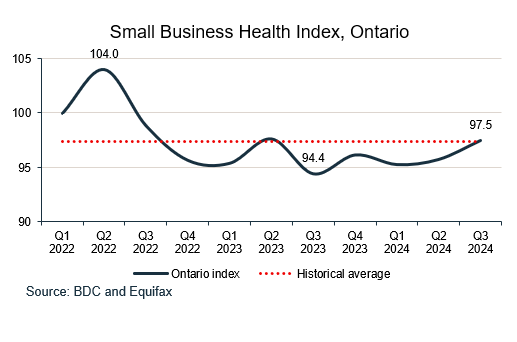

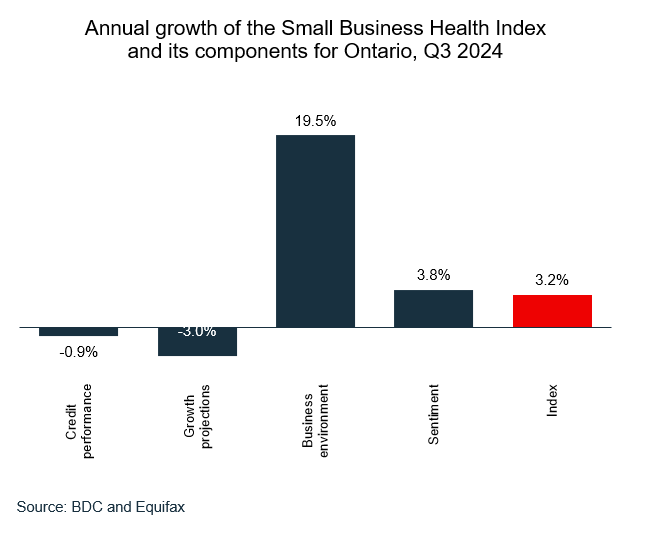

Ontario: Regaining momentum

The health of Ontario small businesses has been improving since the beginning of 2024, reaching 97.5 in Q3 2024—growing by 3.2% year-over-year and 1.8% over the previous quarter.

Ontario’s business environment has seen a 19.5% improvement over the past year and a 14.4% boost in the last quarter, suggesting promising prospects ahead.

Ontario tends to be highly affected by interest rate hikes because of the high concentration of interest rate-sensitive industries and the high level of household indebtedness compared to most other Canadian provinces. The recent cuts should bring further improvements in small business health in the coming months.

Businesses in Ontario were also more optimistic in Q3 2024, with expected improvements in their cash flow and the economy, as well as improved access to credit.

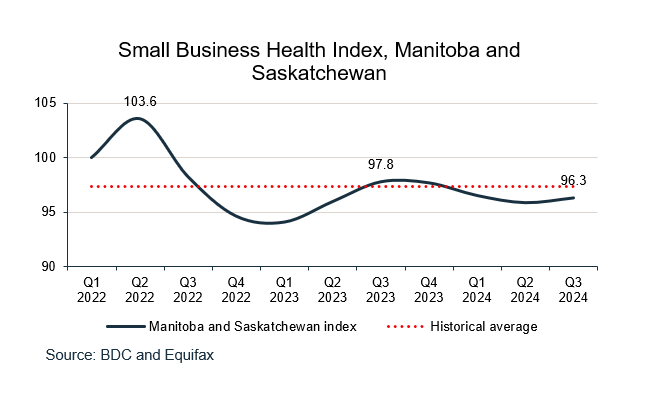

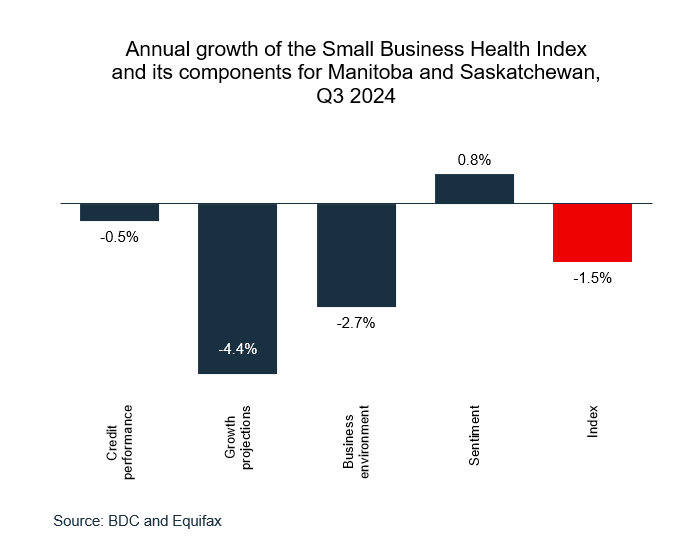

Manitoba and Saskatchewan: Going up and down

Manitoba and Saskatchewan’s index has been going up and down for the past year. In Q3 2024, it stood at 96.3, 1.5% lower than last year but 0.5% higher than last quarter.

Credit performance was down year-over-year, yet it started to recover in the last quarter, suggesting recent improvements in financial performance. Meanwhile, business growth projections and the business environment trended downwards this quarter. Businesses in Saskatchewan and Manitoba had lower investment intentions for the next 12 months, and wage growth slowed compared to a year ago. However, ongoing projects in the mining sector in Saskatchewan could push the index higher in the coming months.

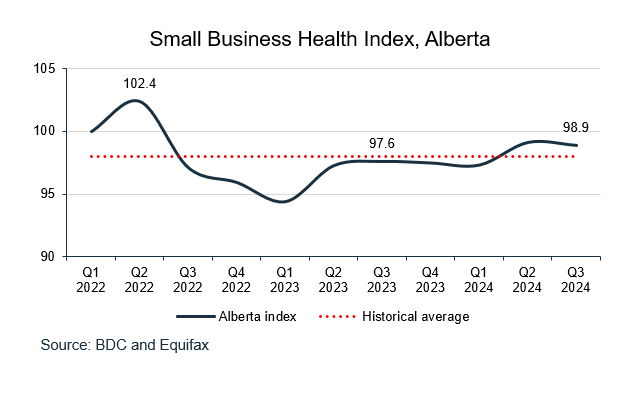

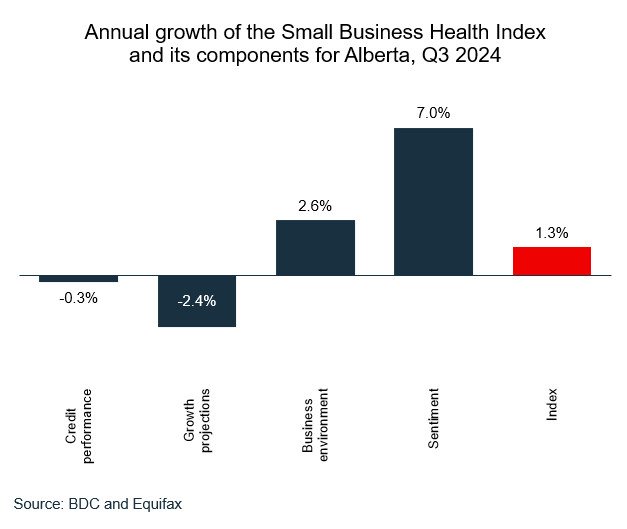

Alberta: Holding steady

Compared to other regions, Alberta small business health was less impacted by the Bank of Canada’s interest rate increases in 2022. Alberta’s economy was more robust in 2023, buoyed by the residential and oil and gas sectors, the latter benefitting from the start of the long-awaited Trans Mountain pipeline expansion. These sectors should continue to support Alberta’s economy and businesses in 2024.

Although the index posted a moderate 1.3% increase year-over-year, now standing at 98.9, it had remained elevated compared to other regions over the last year. There was a small decrease of 0.2% in the Index for Alberta compared with the previous quarter.

Business sentiment in Alberta showed the strongest improvement in Canada, driven particularly by a more positive outlook on the economy. The decline in growth projections was mainly the result of a steady decrease in new credit inquiries and new business openings. However, growing investment intentions could mean businesses will soon take concrete actions to pursue growth opportunities.

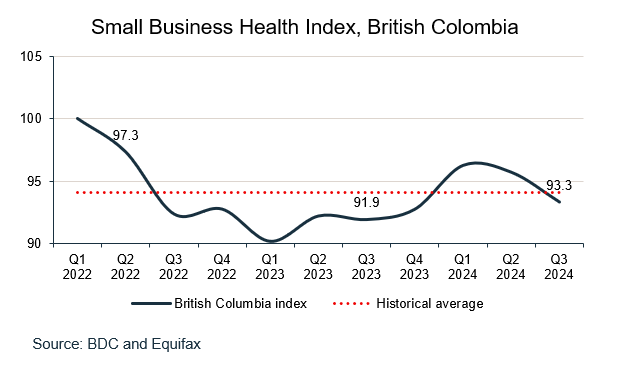

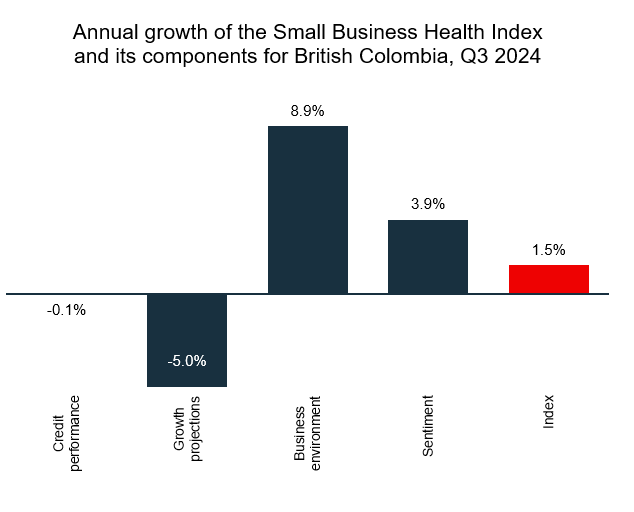

British Columbia: Business health loses some recent gains

British Columbia is trending differently than other regions. While small business health improved at the beginning of the year, it has now reversed course, losing some of its gains.

Despite its 2.5% quarterly decline, the British Colombia index still shows a gain of 1.5% over last year. Still, standing at 93.3 in Q3 2024, the province’s index had the lowest score among the regional indices.

The British Columbian economy has slowed over the past year, and signs of a recovery are still not seen. The province should, therefore, welcome interest rate cuts. British Columbia is more exposed to the housing sector and its population is also the most indebted in the country.

For additional information on the methodology, please consult this document.