Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreInterest rates have begun their descent. Now what?

With the country's inflation rate holding below 3%, the Bank of Canada lowered its key interest rate earlier this month by 25 basis points. Most observers saw this as a sign the bank’s post-pandemic fight against inflation is drawing to a close. However, are a series of rate cuts now a certainty? Can we expect rates to fall as quickly as they rose? In short, how will interest rates evolve over the coming months?

Interest rates are falling mainly because the economy is slowing

Canadian households and businesses are no doubt feeling relief. High interest rates have been a source of frustration and concern for many. After nearly a year at 5.0%, the balance between supply and demand seems to have returned—or so say Canada's central bankers, who have judged the time is right to ease credit conditions.

While this month’s interest rate cut should be seen as good news, the shift in monetary policy is a sign the economy is slowing down.

Indeed, it implies that the high rates introduced to curb inflation by encouraging households and businesses to restrict their spending can now be gradually phased out because the economy has rebalanced sufficiently. Demand has fallen enough to give supply time to adjust in response.

While economic activity is not declining across the country, the pace of growth has weakened. Real GDP growth in 2023 was 1.1%, while the Canadian economy's growth potential is an estimated 2.0%.

The trend of slow but positive growth continued in the first quarter of 2024 and should persist in coming months. It's what’s famously known as a soft landing.

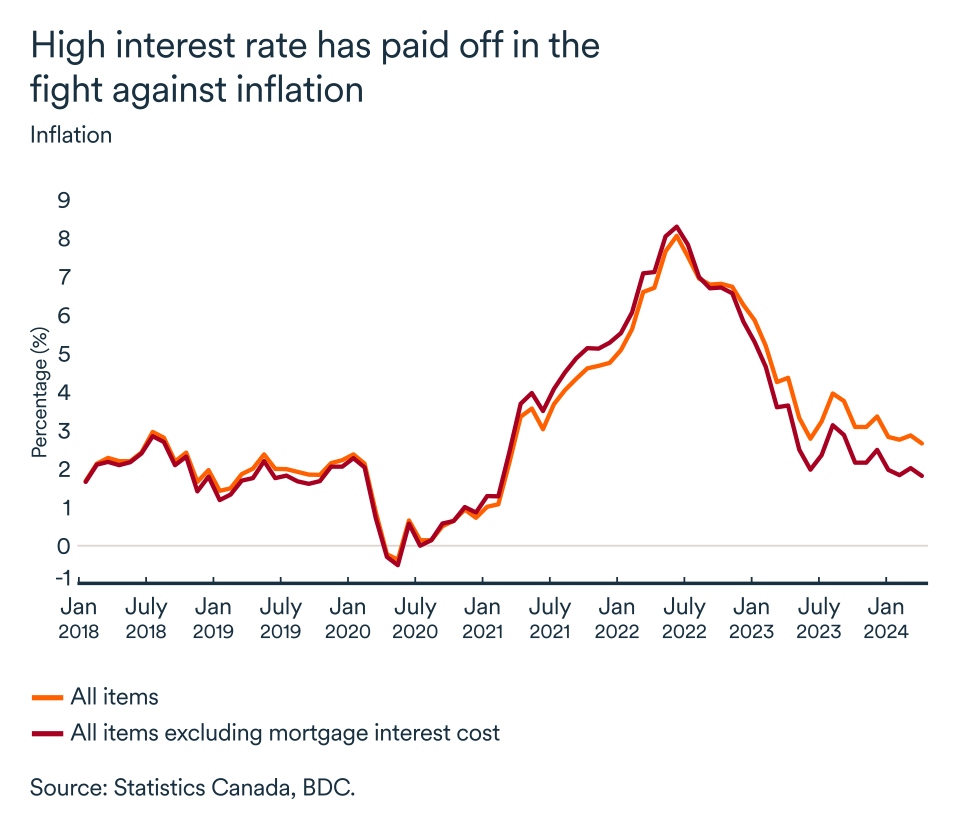

When it comes to inflation, the situation is beginning to return to normal following the price surge caused by the pandemic.

Since the start of 2024, inflation as measured by the Consumer Price Index has remained within the Bank of Canada's target range of 1-3%. Some consumer categories are still experiencing price increases well above what we expected to see in a more balanced economy, notably housing. However, if increases in mortgage interest payments are excluded, inflation would have returned to the 2% target over the past six months on average.

Further reductions are to be expected...

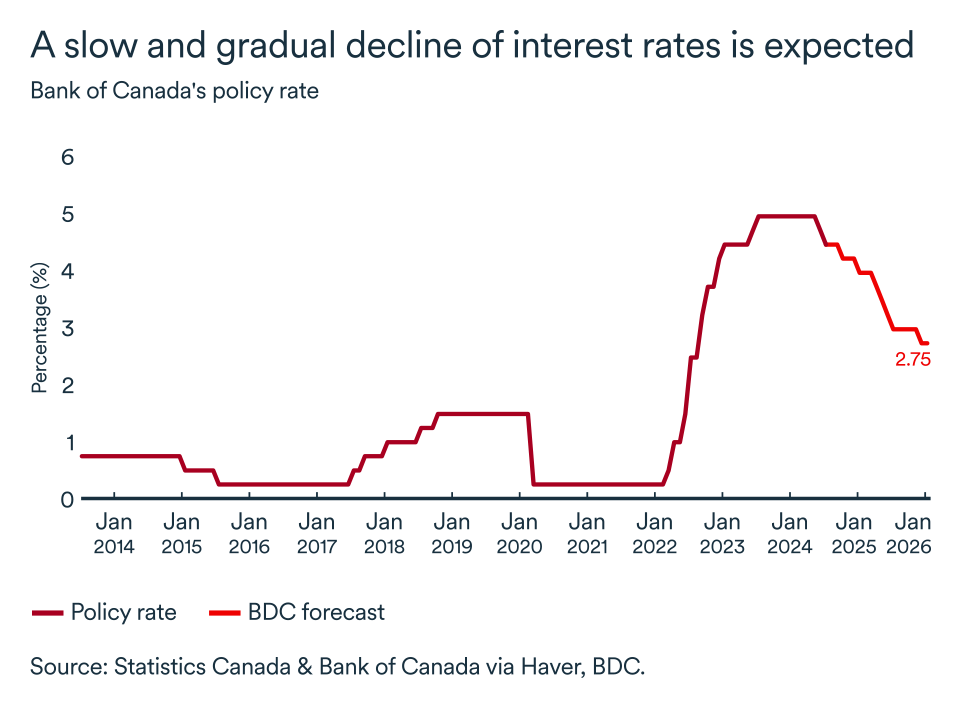

As far as interest rates are concerned, we consider the situation to be "normal" when the key rate is between 2.25% and 3.25%.

Although the Bank of Canada has given no indication of how quickly it will cut, we believe rates could fall by a further 50 to 75 basis points by the end of the year. Our baseline scenario would, therefore, imply a policy rate of between 4.0 and 4.25% in December—still a long way from our estimate for a neutral rate band. The economy will therefore continue to be confronted with restrictive interest rate levels, meaning ones that discourage indebtedness.

Even in the best-case scenario, we shouldn’t expect rates to return to pre-pandemic levels. Global interest rates remained historically low between the great financial crisis of 2008 and the pandemic. However, unless there is a major, unpredictable shock, the key interest rate should fall gradually, until the neutral rate is reached.

Ultimately, we expect the Bank of Canada to bring the policy rate back close to 2.75% (the mid-point of the neutral rate range), but this won't happen until 2026.

In fact, you'd have to go back to July 2022, at the very start of the bank’s post-COVID rate tightening, and October 2008, at the height of the financial crisis easing, to see such low rates. Those were two periods when the economic context was highly unstable and uncertain.

...but the Bank of Canada will be cautious

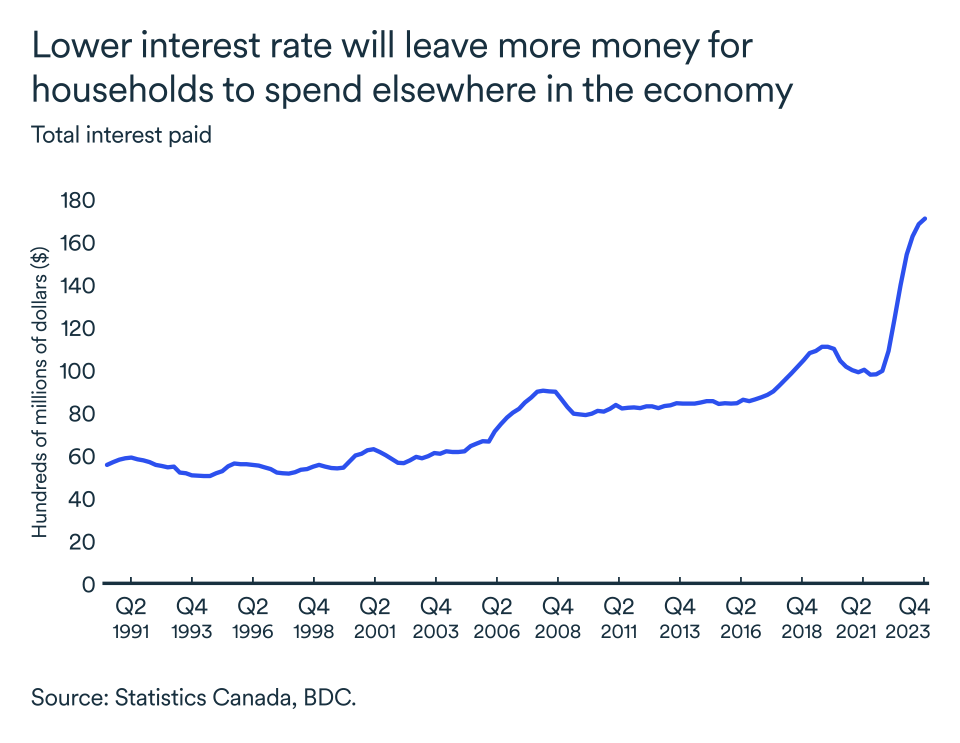

Many companies will be helped by lower borrowing costs, even if the reductions remain modest for the time being. Therefore, this month’s first cut is a cause for optimism and should help restore confidence among consumers and businesses alike.

We can expect it to help the economy regain some strength. Households with mortgages or other variable debt will see their payments fall over the coming months. This will give them more disposable income to devote to consumption, which should boost business revenues

The Bank of Canada will be cautious in its forthcoming decisions for fear that demand will pick up too quickly, resulting in a rebound in inflation. The bank is also faced with structural (i.e., longer-term) issues that it must take into account in its decisions. The housing crisis, climate change and an ageing population will continue to exert pressure on certain prices. These trends will impact businesses costs as well. Companies need to adapt to these potentially profit-threatening trends.

Here are a few tools to help you navigate (still high) interest rates

- Calculate your company's debt-to-equity ratio, as well as other important ratios that banks consider when evaluating loan applications.

- The commercial loan calculator is useful for determining the interest associated with your loan.

Behind modest growth lies strong demand

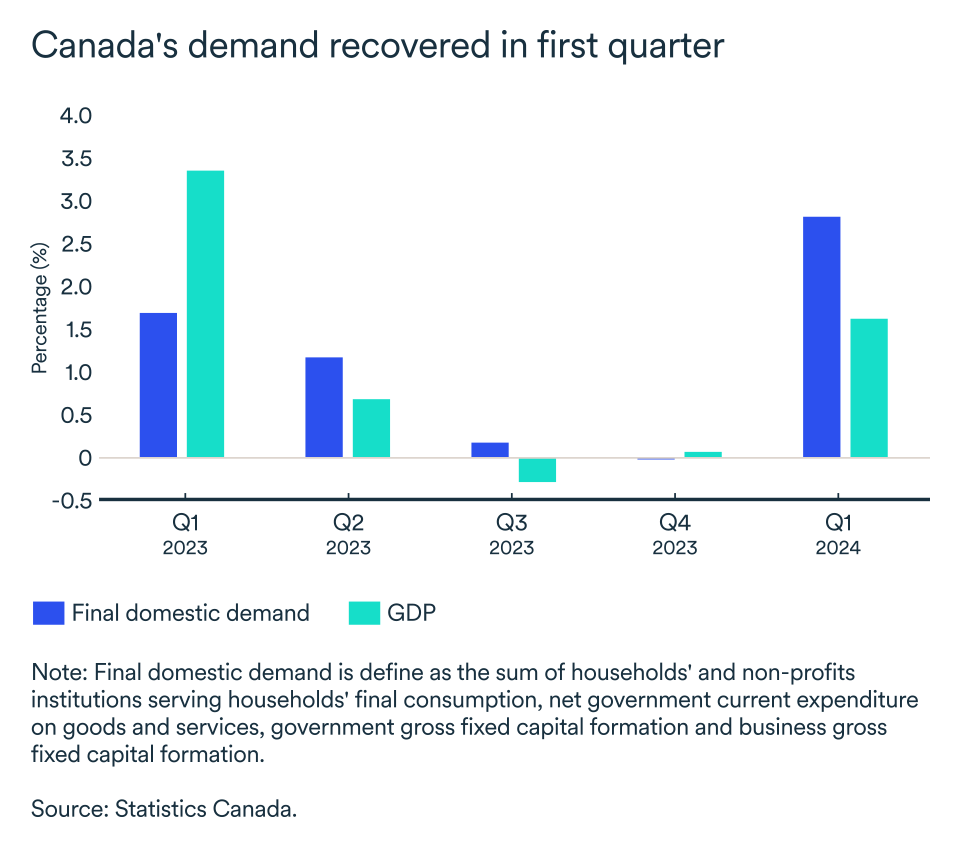

The Canadian economy grew modestly in the first quarter of 2024, but domestic demand saw its strongest quarterly gain in almost two years (before the Bank of Canada began its fight against inflation by raising interest rates in March 2022).

Real GDP, which measures economic activity while accounting for inflation, grew at an annualized rate of 1.7% in the first three months of the year—well below the Bank of Canada's expectations of 2.8% while still a solid performance given the economic context.

Although economic activity stagnated in March, Statistics Canada’s preliminary estimates indicate that monthly growth in April picked up by 0.3%. Growth should therefore continue in the second quarter, although it will likely remain below the economy’s potential—estimated at 2%.

Under the hood in the first quarter

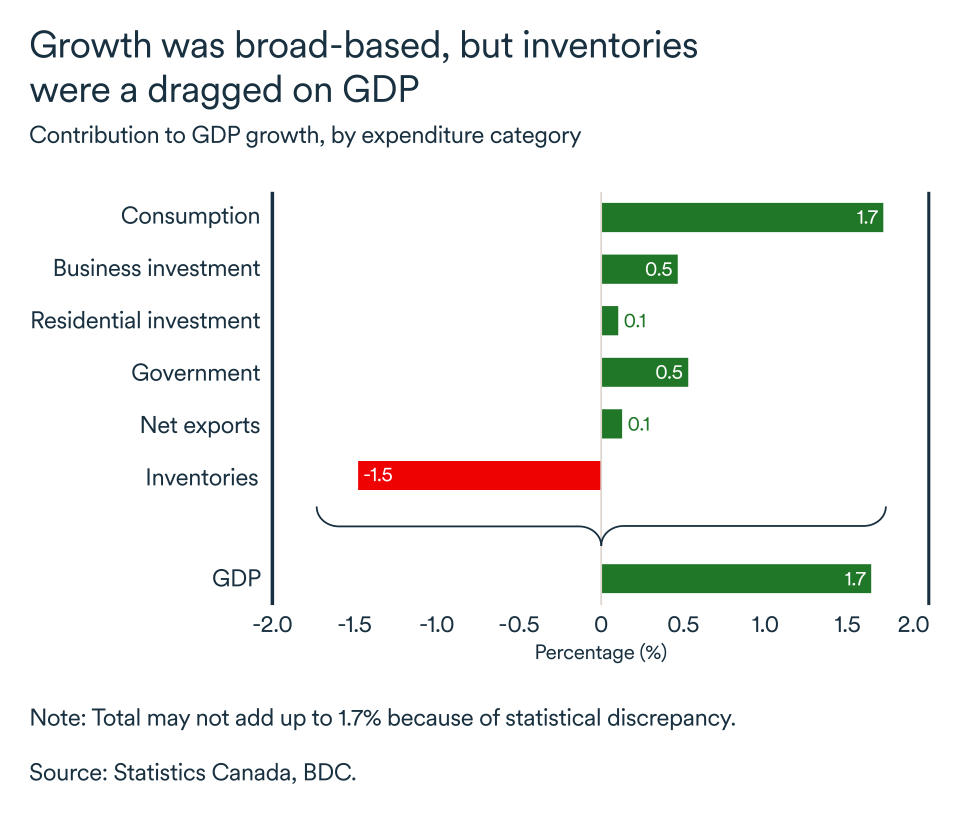

Households and businesses continued to support economic activity at the start of the year. Domestic demand is still very strong. Household spending grew at an annualized rate of 3.0% in the first quarter, similar to the last quarter of 2023. Purchases of services led the way, but consumers also spent more on goods, notably new trucks, vans and sport utility vehicles. Even when population growth is taken into account, per capita consumer spending increased after several quarters of decline.

Businesses also contributed to growth at the beginning of the year. Non-residential investment rose by 4.3% compared with the fourth quarter of 2023. Most of the weakness in GDP can be attributed to lower business inventories. Inventories reduced GDP growth by 1.5 percentage points as companies struggled to clear excess stock sitting on their shelves and in warehouses. Although the inventory drawdown was widespread, it was most pronounced in the automotive sector.

Savings on the rise despite persistently high interest rates

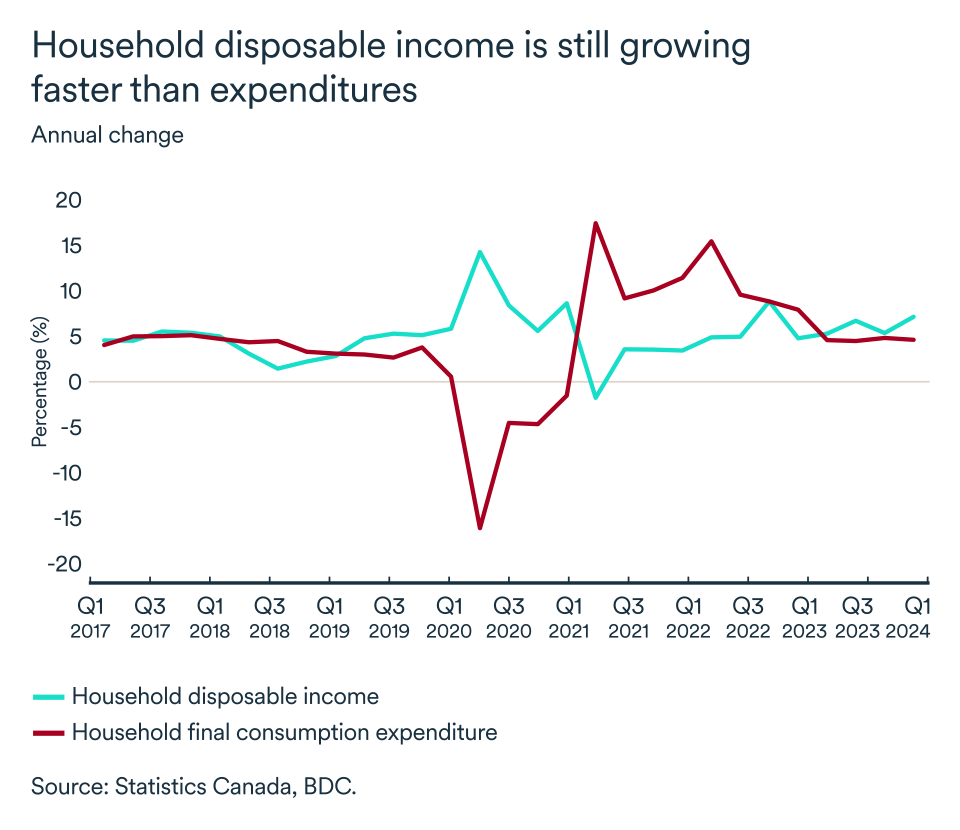

An increase in disposable income (up 1.8% over the last quarter) and the expectation of lower interest rates in the coming months probably helped boost household confidence, which partly explains the healthy growth in spending.

Nevertheless, consumers were able to save more. The household savings rate stood at 6.9%, another peak in almost two years.

Surprisingly, Canadians didn’t have to dip into their savings to pay for purchases. Rising salaries and investment income were sufficient for households to continue supporting the economy.

Employment holds up in May

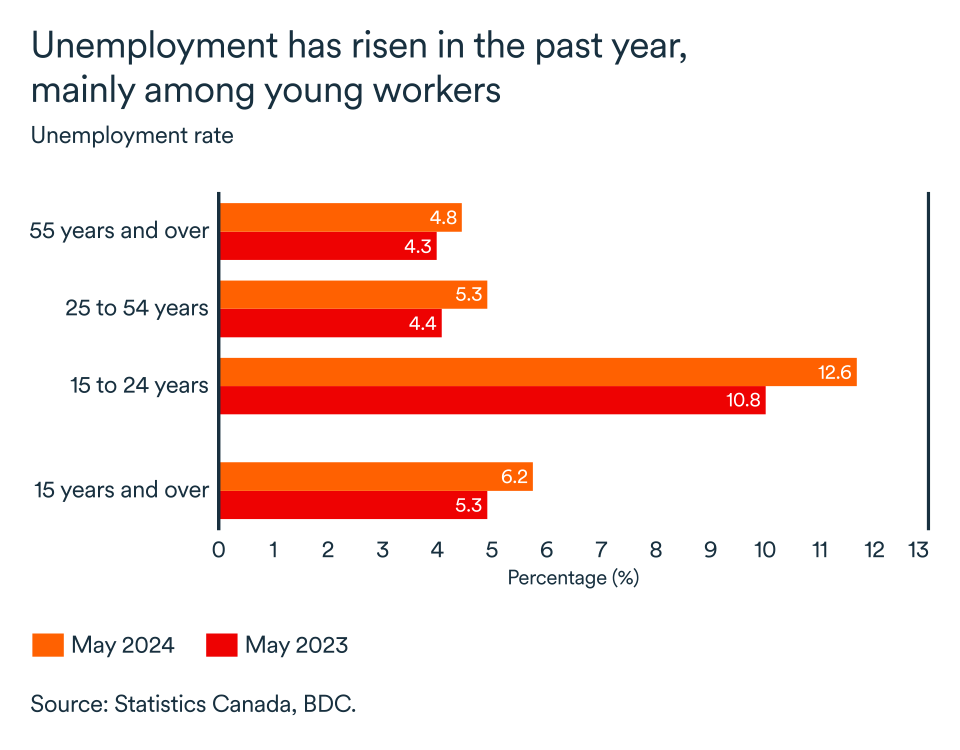

After April's significant job gains (+90,000 over a single month), employment gains slowed in May. The increase of 27,000 jobs last month means the Canadian economy has created 38,600 jobs on average every month since the start of the year. This is largely in line with 2023 when some 35,000 jobs were created per month on average.

The unemployment rate continued to rise, now standing at 6.2%. Unemployment increased most among younger workers, while unemployment among the core age group (25-55) remains among the lowest in Canadian history.

Job vacancies continue to trend toward normal. While the number of available jobs remains high, the majority are in industries dominated by the public sector, such as health care and education.

Overall, the labour market continues to normalize, but growth in average hourly earnings is still rising faster than the Bank of Canada would like to see, at a rate of 5.1% in May compared with the same period last year.

What does this mean for your company?

- The stability of interest rates for almost a year now seems to have given consumers time to adjust to higher debt servicing costs as they continued to increase their spending. Now that the Bank of Canada has announced its first rate cut, credit conditions will continue to ease over the coming months, boosting households' propensity to spend and keeping the economy strong.

- Robust growth in domestic demand in Canada at the start of the year, however, points to higher interest rates for longer, which will keep up the pressure on business costs. Find out how to manage your costs more effectively.

- A significant slowdown in inventory investment could also point to a resurgence of inflation in the second half of the year. In addition to the strength of the economy, which should pick up again following this month’s rate cut, companies may also have been trying to sell off their inventory at a discount at the start of the year.

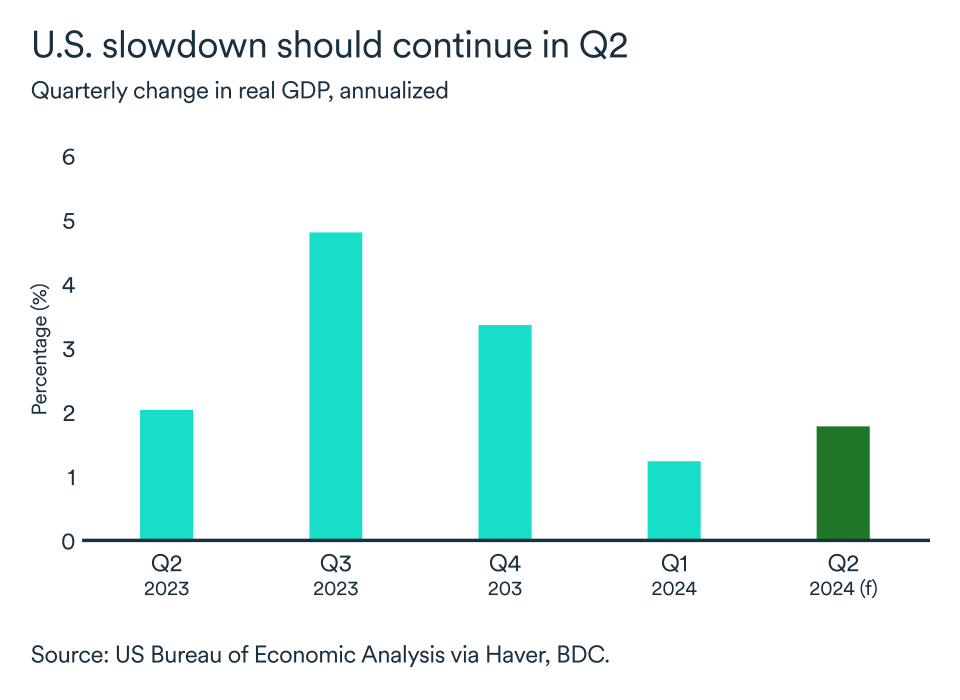

The slowdown deepens in the United States

The U.S. economy grew by 1.3% in the first quarter, according to the latest estimates from the Bureau of Economic Analysis. This was a downward revision from initial data released last month and mainly reflects weaker consumer spending.

A slowdown in the economy that began at the start of the year is set to continue in the second quarter, with real GDP now expected to grow by 1.8% compared with the first quarter.

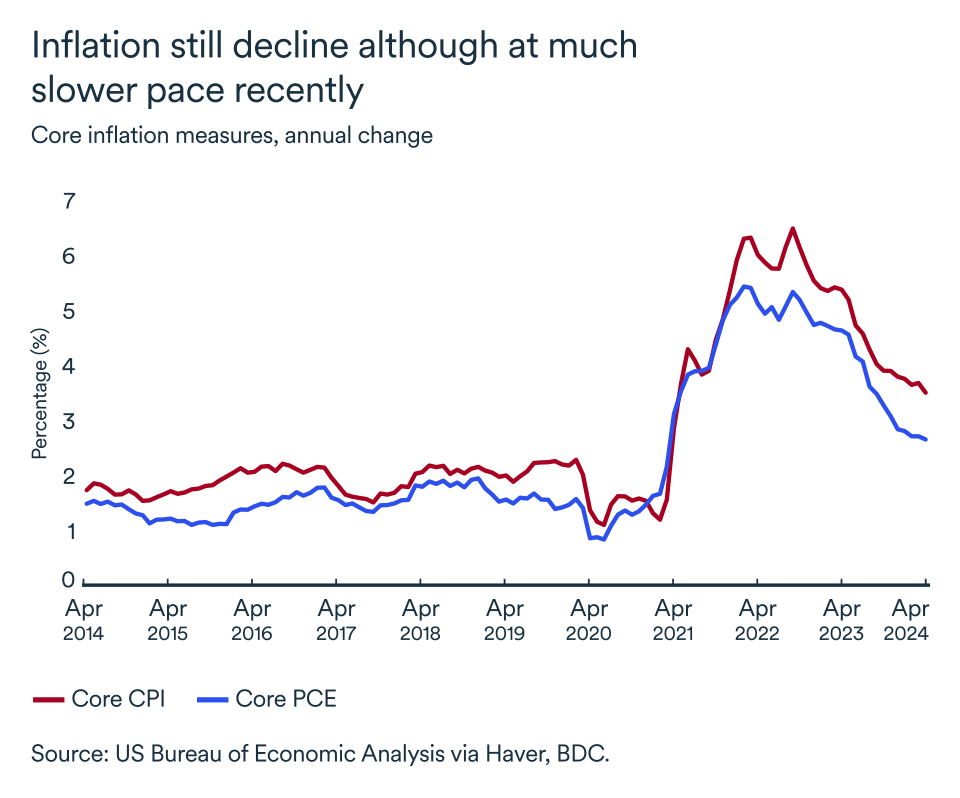

Inflation back on track

A resurgence of inflation in March didn’t continue into April, but progress was meagre, regardless of the inflation measure used. There was improvement in the monthly inflation data for basic services and housing rentals—two categories where price growth has been especially stubborn. However, it will take much more slowing to bring inflation back to target.

Inflation as measured by the core Personal Consumption Expenditure (PCE) price index, the measure on which the Federal Reserve’s 2.0% target is based, came in at 2.8% in April. This was a negligible decline from the previous month.

The Fed generally places more emphasis on the PCE index than the core consumer price index, which improved to 3.6% from 3.8% in March.

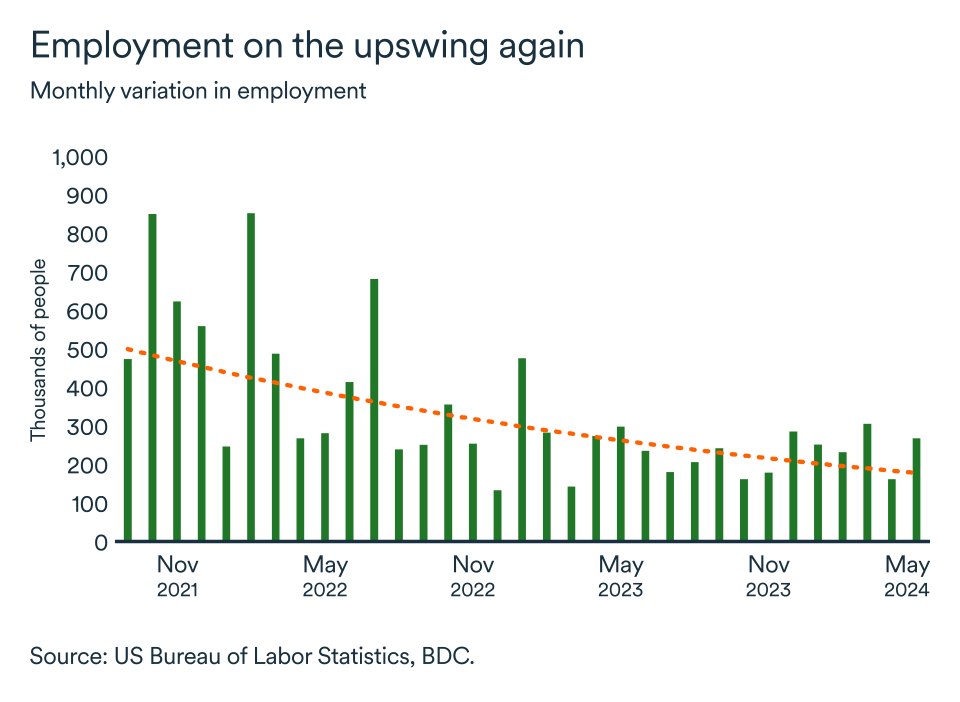

The job market shows increasing signs of moderation

In recent months, the job market has slowed, but this appears to be more of a rebalancing than a cause for concern for the U.S. economy or Federal Reserve policymakers. Employment rose by 270,000 jobs in May and the unemployment rate increased to 4.0%.

Average hourly earnings continue to normalize, rising by 3.7% year-on-year. The number of jobs available declined to 8.06 million in April from 8.36 million in March, according to the Bureau of Labor Statistics.

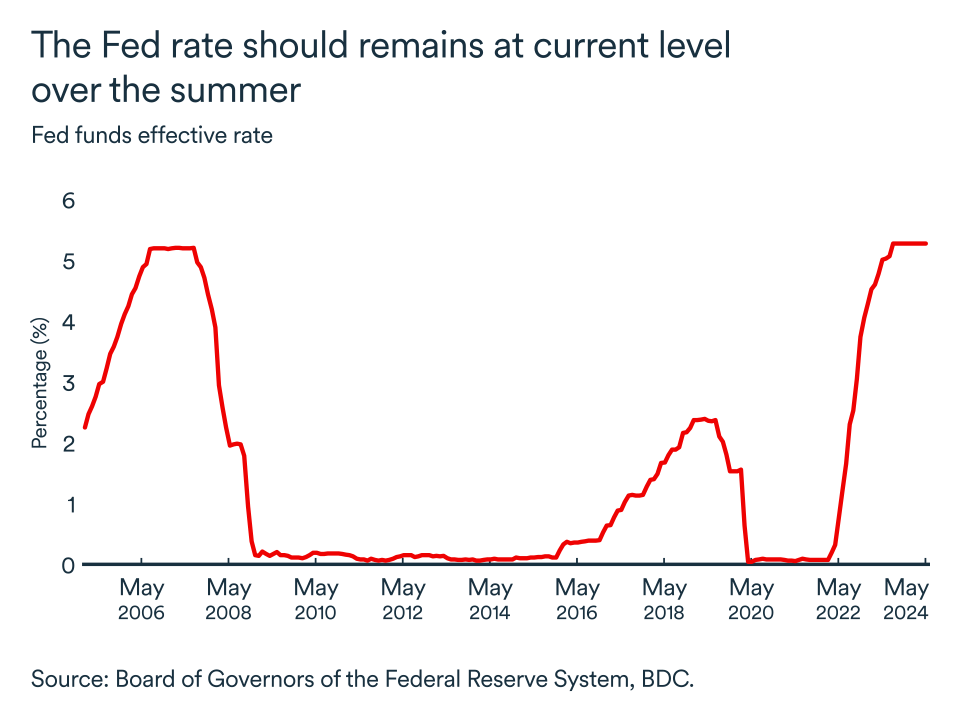

Americans will have to be patient for rate cuts

At its June meeting, the Chair of the U.S. central bank, Jerome Powell, announced the bank had once again decided to hold its trend-setting rate steady. The overnight rate will remain at 5.25-5.50%, at least until the end of July.

High inflation, a resilient economy and a still-strong labour market do not augur well for a quick easing of monetary policy. Even if these three factors are all pointing in the right direction, the Fed is likely to want to see more stabilization in the economic data before lowering the federal funds rate due to the risk of rekindling inflation. Most observers believe the Fed is unlikely to lower rates before September.

A word on Donald Trump's conviction

Although historic, the conviction of former President Donal Trump is unlikely to have a significant impact on the U.S. economy.

The impact on your business

- It may have taken longer in the U.S. than elsewhere, but it seems that the tightening of monetary policy is finally slowing the real economy. The slowdown is being felt in goods consumption and business investment. If the U.S. is an important market for you, you may soon feel the impact.

- Stable interest rates in the U.S. and the slowdown in the Canadian economy could push the Canadian dollar lower over the summer, favouring exports.

- Employment continues to perform well, although it’s showing signs of moderation. The continued health of the labour market will help sustain some consumption in the months ahead, despite persistently high interest rates.

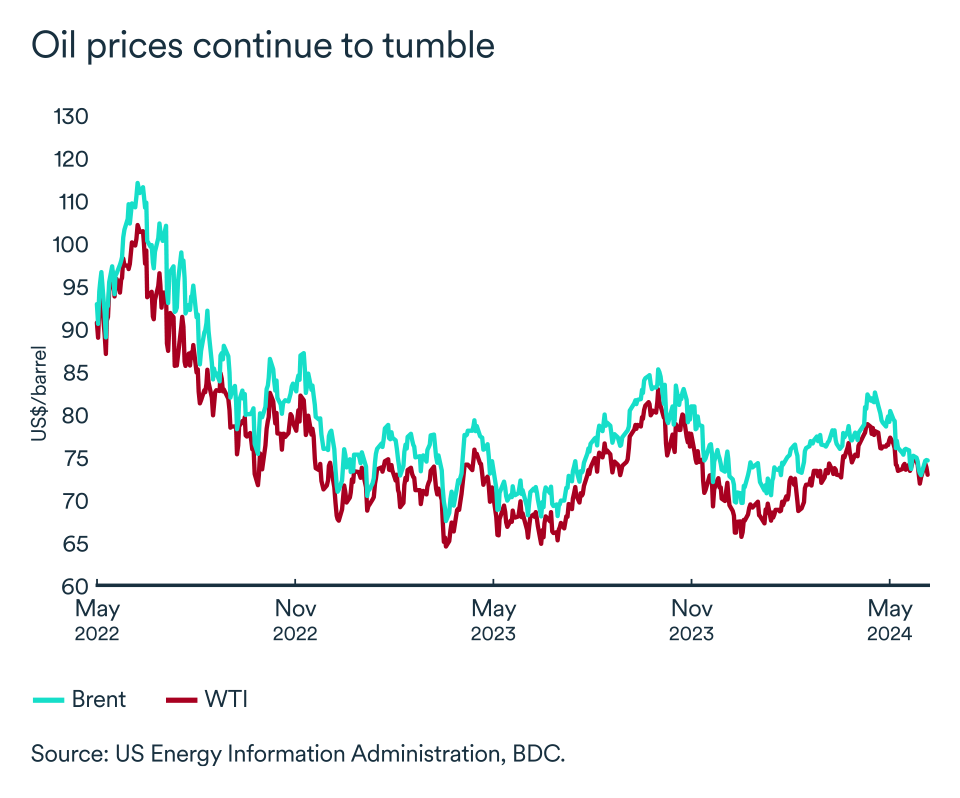

Prices fall as OPEC+ agrees to bring supply to market

Brent crude fell by more than 3% in June, bringing the oil price to below US$80 a barrel, its lowest level since February.

The Organization of the Petroleum Exporting Countries and its allies (OPEC+) announced this month an extension of production cuts until 2025. However, the cartel also agreed that voluntary cuts would be phased out beginning in October, market conditions permitting.

This means that supply from OPEC+ will increase as voluntary cuts come off, but the scenario depends on the global economy strengthening in the wake of expected interest rate cuts, especially in the U.S.

The announcement had a significant effect on futures contracts. The majority of total reductions are currently coming from the voluntary program. Total reductions are 3.66 million barrels per day (bpd), of which 2.2 million bpd comes from the voluntary program, equivalent to around 60% of reductions.

The United Arab Emirates, which has been pressing for an increase in production for several months now, succeeded in having its quota revised upwards immediately. Oil supply should, therefore, begin to increase in the next few days, even as monetary policies around the world remain restrictive and economic growth modest.

Is the market balanced?

The recent volatility of the main crude benchmarks has been largely dictated by geopolitical risks. Prices have also been influenced by the production cuts.

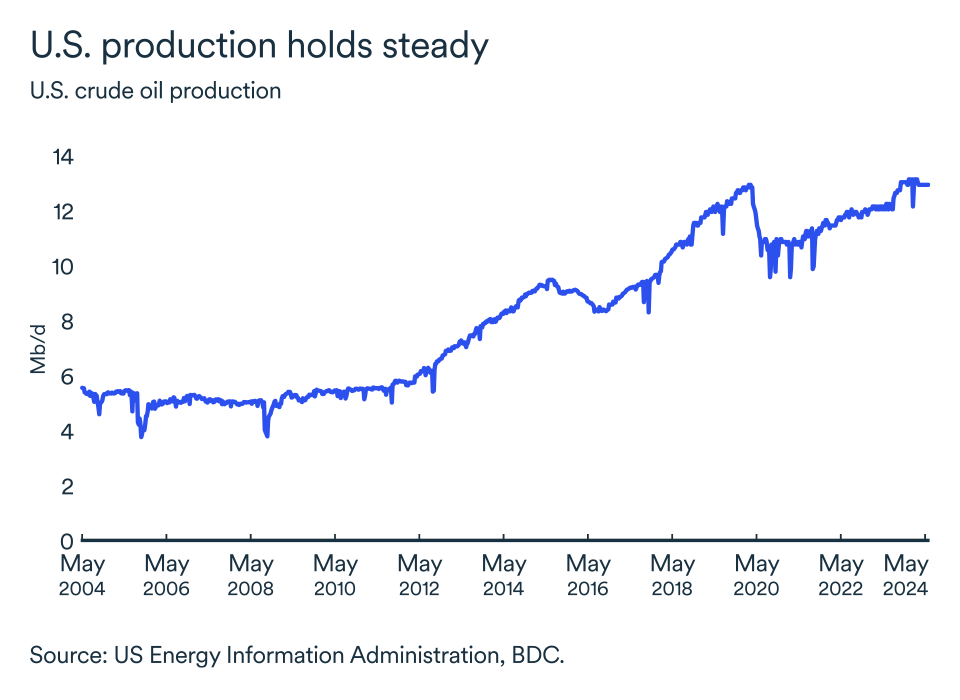

The U.S., thanks to the shale revolution and technological advances, has been the driving force behind growth in non-OPEC+ global oil supply over the last decade, but U.S. producers have become less aggressive in recent years.

Indeed, total U.S. crude production has changed little since the beginning of the year. In April, it stood at around 13.13 million bpd, down slightly from 13.26 million bpd at the end of 2023.

According to OPEC's May forecasts, global oil demand is set to increase by 2.2 million bpd this year. This level would outstrip the increase in oil supply from non-OPEC+ producers, which is estimated at around 1 million bpd. As a result, demand for OPEC+ crude oil would have to be around 900,000 bpd higher than in 2023 to maintain the market at recent prices.

Bottom line...

Crude oil prices will continue to move in step with the global economy. Prices have fallen recently, mainly due to fears that supply will outstrip demand. However, OPEC and its allies believe the context is conducive to an increase in supply, and therefore intend to return barrels to the world market this autumn. The oil market is betting on an increase in demand for crude in response to widespread interest rate cuts across the globe expected this summer.

The Bank of Canada cut its policy rate for the first time since 2020

The Bank of Canada announced a 25bps reduction in interest rates on June 5th, marking the first rate cut since 2020. This decision comes after a weaker-than-expected first quarter growth of 1.7%, and headline inflation remaining within the target range over the past few months. The central bank stated: “the economy is in excess supply, there is room for growth even as inflation continues to recede”. Looking ahead, the Bank will adopt a gradual and cautious approach, closely monitoring incoming data related to inflation and growth to decide on its next move.

We anticipate that the Canadian economy will continue to run below potential for the remainder of the year and that inflation will continue to ease allowing for further rate cuts. By year-end, interest rates are expected to be in the range of 4.0% to 4.25%.

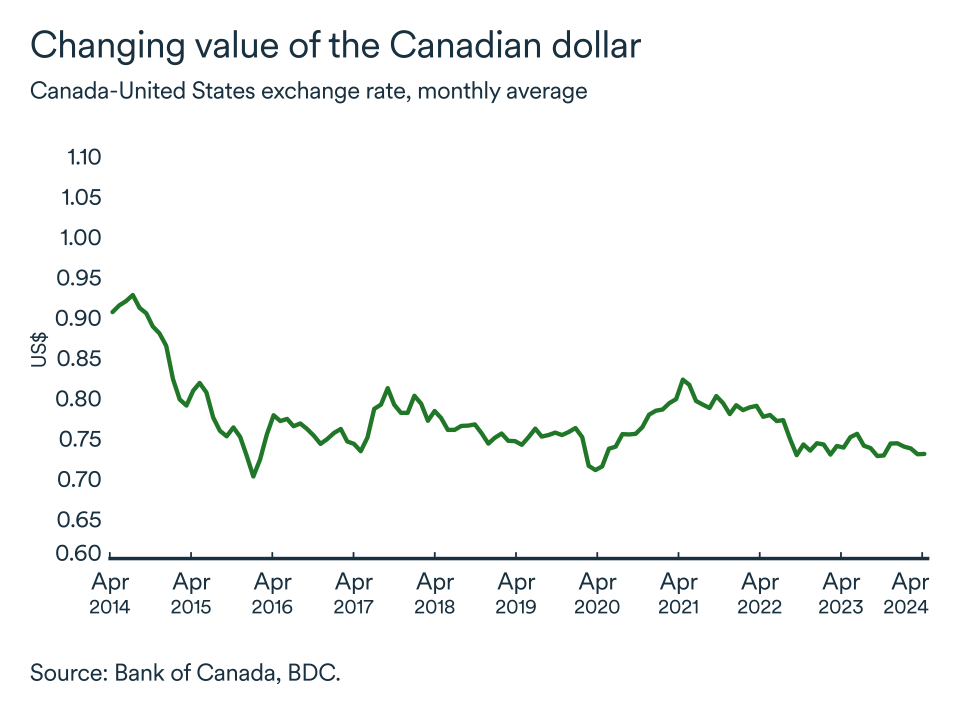

The Loonie was stable in May

In May, the Canadian dollar remained stable, averaging US$0.73, consistent with previous months. The Canadian dollar is expected to face continued pressure throughout the year. On the US side, the Federal Reserve is expected to start loosening its monetary policy around fall, the US economy is resilient and is expected to outperform its trading partners, resulting in a stronger U.S dollar.

However, a weaker exchange rate supports the competitiveness of Canadian exports. We expect the exchange rate to fluctuate between US$0.72 and US$0.75.

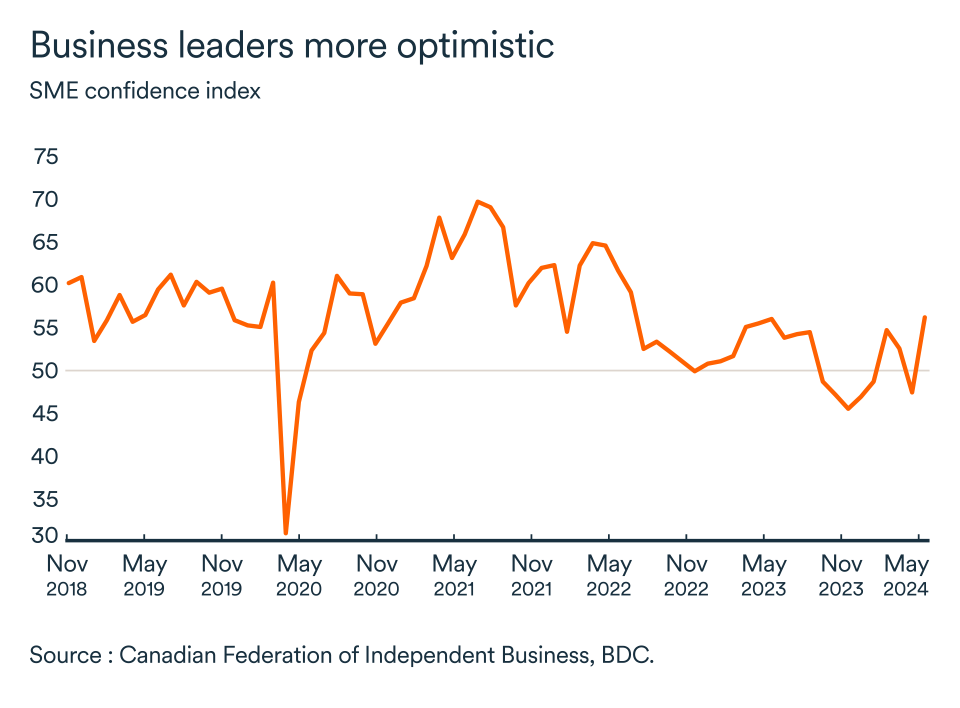

Confidence recovered in May

The CFIB's confidence index for the year ahead recovered in May. Optimism increased from 47.5% to 56.4% between April and May, marking a significant shift in sentiment among business leaders.

Confidence varied among provinces: Ontario’s gained significantly in optimism, driving the Canadian average higher. However, some provinces were less optimistic such as Alberta, Saskatchewan, and the Atlantic provinces.

We expect confidence to continue to improve as inflation continues to ease and further rate cuts materialize, alleviating borrowing and input costs on businesses.