Tangible and intangible assets

In accounting, an asset is defined as a current economic resource that has the potential to produce economic benefits. It is recorded on the balance sheet only if it is likely to produce future economic benefits.

Assets may be tangible or intangible. An intangible asset is a non-monetary asset that cannot be seen or touched. “Patents or goodwill are good examples,” says Florence Bessette, Business Advisor, BDC Advisory Services. Tangible assets are physical things. Examples include land, buildings, vehicles, furniture, and equipment.

On the balance sheet, assets are recorded as current and long-term assets (non-current assets). Current assets include any assets that the entity expects to realize, sell or consume in its normal operating cycle, holds for trading and expects to realize within 12 months of the reporting date, as well as available cash. All other assets are recorded as long-term assets.

Current assets are generally tangible assets, while long-term assets can be tangible or intangible.

What are tangible assets?

A tangible asset is an asset that has physical substance. Examples include inventory, a building, rolling stock, manufacturing equipment or machinery, and office furniture. There are two types of tangible assets: inventory and fixed assets.

Examples of tangible assets

- Inventory

- Raw materials

- Goods in process

- Finished products

- Fixed assets

- Equipment

- Office furniture

- Rolling stock

- Computer equipment

- Land

- Building

- Leasehold improvements

Fixed assets are tangible assets that are used to produce goods or provide services, or for rental or administrative purposes. They are intended to be used on a long-term basis and will be recorded as long-term assets on the balance sheet.

What are intangible assets?

An intangible asset is a non-monetary asset that has no physical nature. It cannot be touched or felt.

Monetary assets are financial assets, such as cash, accounts receivable and investments, because they represent an entity’s right to receive cash or another financial asset from another party, the customer.

Examples of intangible assets

- A trademark

- Goodwill

- Patents

- Software

- Internally generated intangible assets (during the development phase)

What is the difference between tangible and intangible assets?

One of the biggest differences between tangible and intangible assets is how they are valued. This is because tangible assets normally have a finite life. Rolling stock is a good example of equipment that wears out over time and has a limited lifespan—not always the case for intangible assets, such as the trademark of an acquired entity.

Further, the purchase or creation of a tangible asset is not an expense since it is listed as an asset on the balance sheet. The value of that asset is then amortized over time.

Meanwhile, intangible assets, such as a company’s brand, will not appear on a balance sheet. What went into creating them will be recorded as an expense in the income statement. When a company is purchased, the price paid for assets that do not appear on the balance sheet is recorded as goodwill on the acquirer’s balance sheet.

Valuing fixed assets

Fixed assets are the most common type of tangible assets. Because the company holds fixed assets for long-term use, their acquisition cost is amortized. The company can use either the straight-line or declining balance method to amortize categories of fixed assets.

Land, which is a tangible asset, is never amortized because its life is unlimited.

To reflect wear and tear on its rolling stock, for example, as well as the rate at which revenue will be generated from its use, a company might decide to amortize the cost of a tractor-trailer on a declining-balance basis, at a rate of 30% per year, because it believes that as the tractor-trailer is used, it will be less productive and will require more maintenance and repair, and thus produce less economic benefit for the company.

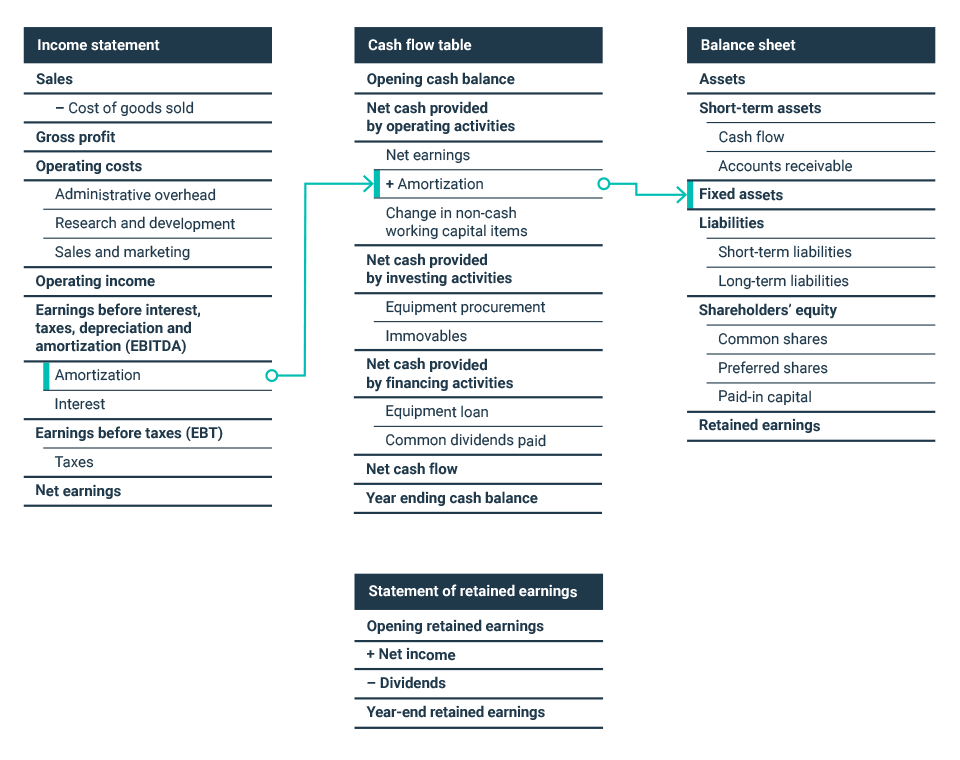

The balance sheet will then report the net book value of the asset (i.e., its acquisition cost less accumulated amortization), while the income statement will show the annual amortization expense. The amortization expense for the previous year will be included in retained earnings, under shareholders’ equity. The image below shows these links between the various financial statement documents.

Example of a declining balance amortization

In a straight-line amortization, the price of an asset is divided by the number of years it is expected to be useful. The amount amortized each year is equal from one year to the next until the value of the asset reaches zero.

In a declining balance amortization, the amortization expense will be smaller in subsequent years.

“Let’s say a company buys a tractor-trailer at a cost of $100,000 at the beginning of fiscal year 2020,” says Bessette. “It decides to amortize it on a 30% declining balance basis. During the first year of use, the $100,000 cost will be amortized at a rate of 30%.”

The company will therefore record the net book value of this asset at $70,000 in the year of purchase on the balance sheet under long-term assets, and will add a $30,000 annual amortization expense in that same year on the income statement.

In the following fiscal year, the amortization expense recorded in the income statement will be $21,000 ($70,000 x 30%). On the balance sheet, the net book value will be $49,000, which is the $100,000 cost, minus the $51,000 accumulated amortization.

If the company had instead chosen to amortize the same asset on a straight-line basis over five years, the annual amortization expense recorded in the income statement would have been $20,000 per year until the end of its useful life.

| Year | Amortization (expense in the income statement) | Accumulated amortization | Net book value (recorded on the balance sheet) |

| 1 | $30,000 | $30,000 | $70,000 |

| 2 | $21,000 | $51,000 | $49,000 |

| 3 | $14,700 | $65,700 | $34,300 |

| 4 | $10,290 | $75,990 | $24,010 |

| 5 | $7,203 | $83,193 | $16,807 |

Valuing intangible assets

Unlike tangible assets, some intangible assets do not have a useful life. “Take a trademark that’s been acquired, for example” says Bessette. “A trademark has no lifespan. It will exist as long as the company does. It is therefore difficult to amortize the cost of this trademark to reflect its use.”

Since it cannot be amortized, the intangible asset will be carried at cost and then impaired if there is a loss of value (an impairment is a reduction in the book value of an asset). Let’s look at two examples.

- Trademark

First of all, it is important to differentiate between a trademark developed internally and a trademark acquired through a business acquisition. An internally developed trademark is never recognized in financial statements because it does not meet the criteria for recognition as an intangible asset. For an intangible asset to be recognized in the balance sheet, it must be separable from the entity that develops it, which is not possible in this case. When an entity operates a business, it incurs various operating expenditures. It is therefore very difficult to evaluate the cost of developing the trademark separately.

However, Bessette says the value of an externally acquired trademark can be assessed. A portion of the purchase price of the business will be allocated to the trademark at the date of the transaction. This will require the services of a business valuation specialist.

“You often have to bring in specialists to perform this kind of valuation” says the business consultant.

- Goodwill

Goodwill refers to the value a company gets from its brand, customer base and reputation associated with its intellectual property. Goodwill is a long-term asset that generates value for a company over a number of years.

As with trademarks, it is very difficult to assess the useful life of goodwill. For this reason, accounting standards state that goodwill does not have a finite life.

In order to evaluate goodwill in financial statements, the company will then have to determine its fair value by performing an impairment test.

“Suppose we buy a company, but it starts losing money, customers and market share, and generates operating losses,” says Bessette. “It is advisable to take a critical look at the valuation of goodwill. We may have paid too much to buy the shares of this company. To avoid overvaluing the asset, an impairment test will be performed.”

This will allow the company to determine whether the loss should be recorded in the income statement related to goodwill. The company will recognize a loss if the carrying value of goodwill exceeds its fair value. For example, one method used to calculate the fair value of goodwill is to discount the estimated and expected future cash flows (i.e., the cash inflows and outflows from the operation of the acquired business).

Are there as many tangible and intangible assets in all industries?

The number of tangible and intangible assets held by companies can vary significantly between industries.

A manufacturing company will generally have more tangible assets. It will have fixed assets, such as property, plant (if it decides to buy rather than lease the space) and inventory. A service business, whose main expense is labour, will have relatively more intangible assets, some of which may not be on the balance sheet, such as customer lists.

Florence Bessette

Business Advisor, BDC Advisory Services

Because a service sector firm normally has fewer tangible assets, the firm may find it more difficult to secure financing. In these cases, banks will not accept a real estate or chattel mortgage. They will require other types of collateral for their loans.

Understand your financial statements

Depreciation is a key concept in understanding your financial statements. Learn more to understand your financial statements and inform smart business decisions. Download our guide.