Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreThe job market is rebalancing—what will be the impact for companies?

Despite maintaining positive growth, the Canadian economy continues to slow. In April, the national unemployment rate stood at 6.1%—the highest since the end of the pandemic.

When the labour market eases, we normally expect wage growth to also slow, as bargaining power shifts to employers. However, we have yet to see a significant deceleration in wages, probably because of structural changes in the economy that will continue to influence the labour market. Will business leaders get a break on wages this year?

Labour shortages becoming rarer

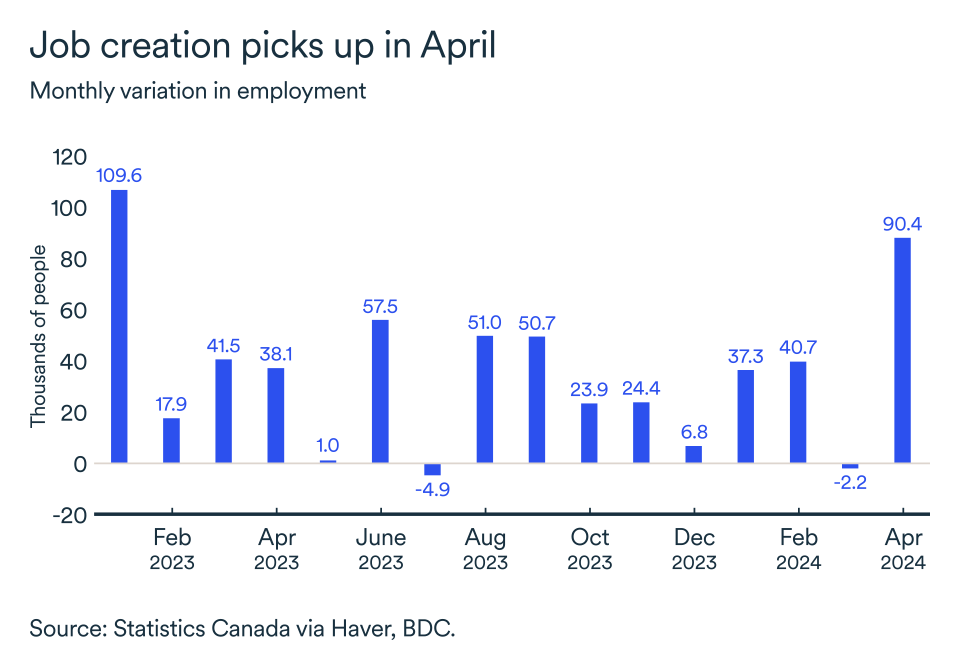

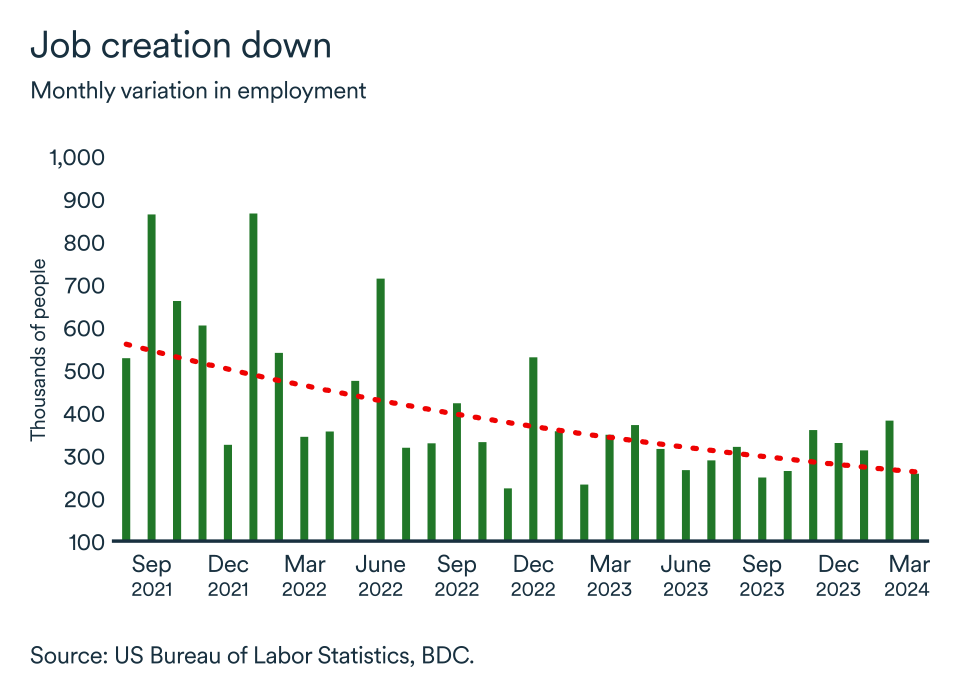

Employment remains solid. Since the start of 2024, an average of 41,500 jobs have been created per month, compared with a monthly pace of 35,000 in 2023. Nonetheless, there are signs of easing of labour market conditions which reflects both lower demand for new workers and a greater supply of potential employees. The larger supply of workers is coming from several sources.

The departure of the baby-boom generation will weigh on the workforce until at least 2031, when the last of its members reach age 65. However, retirements have so far been slower than expected, with the number of boomers working past age 65 continuing to grow.

Companies have increasingly turned to newcomers to meet their labour needs in recent years. This category of worker represents an important source of new employees. Indeed, without immigration, Canada's labour force would see little or no growth this decade. After a drop during the pandemic, immigration is set to increase significantly between 2022 and 2025, with the annual immigration rate projected to hit around 1.1% over the period.

With the economy slowing, layoffs have increased although not to alarming levels.

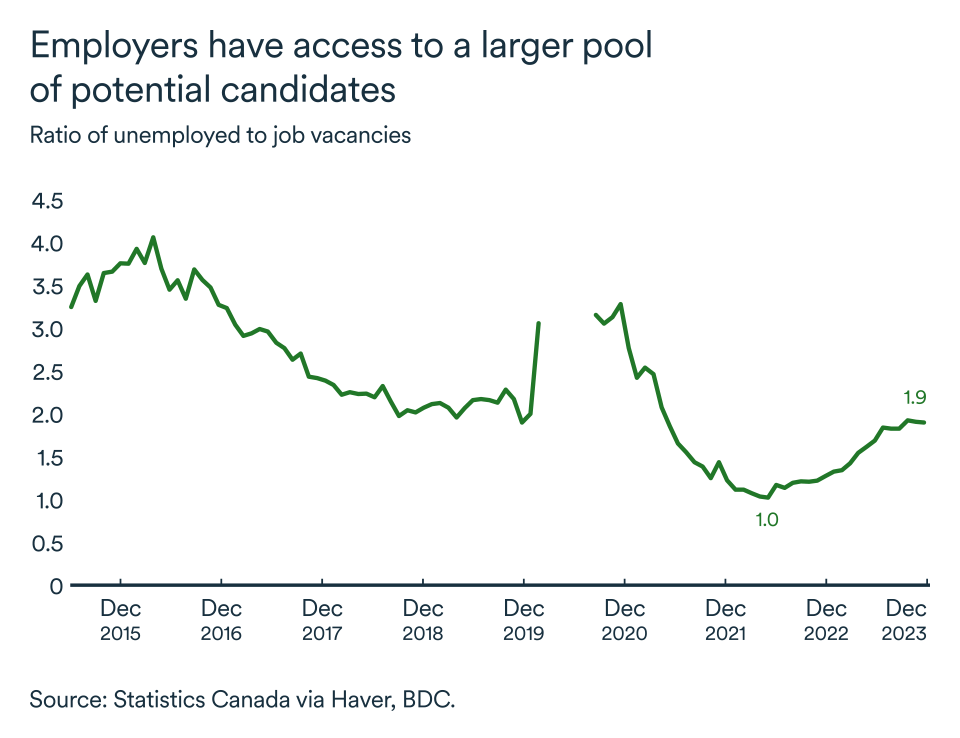

These factors have meant the pool of potential workers has grown faster than new job creation. Job vacancies began to decline in the second half of 2023. Employers, therefore, have more options for finding replacement workers and filling new positions.

Despite this ongoing rebalancing, the Canadian labour market remains robust. At the start of the year, 43% of companies were planning staff increases, and there were almost 660,000 job vacancies across the country in February.

Still, the pace of job creation is normalizing, easing the pressure on the labour market. Only 22% of companies surveyed by the Bank of Canada report production difficulties due to staff shortages. The historical average is 31% and, therefore, we’ve seen a clear improvement for companies.

Does this mean smaller salary increases?

The latest national employment report showed that the average hourly wage rose by 4.7% year-on-year in April. While it takes time for wages to return to normal levels after a bout of inflation, the process has likely been slower this cycle than many employers (and probably the Bank of Canada) had hoped.

Although companies generally expect salaries to increase at a slower pace than in the last two years, many firms continue to believe wage growth will remain high. The proportion of companies expecting abnormally high wage growth to persist until 2025 has risen from 14% at the end of 2023 to 23% in 2024. This is a sign that employers are still feeling pressure from workers for higher pay.

Expectations of substantially higher wages by workers was confirmed in a recent Bank of Canada report. It found that although private sector employees still expect higher wage increases than public sector employees, wage expectations are rising faster among the latter group.

Moreover, Canada is targeting a decrease in temporary resident population. Therefore, pandemic measures to ease the labour market conditions are getting undo. Stricter access to limit the number of temporary workers will undoubtedly have an impact on business owners who have been relying on the program for the past years. As the share of low-wage workers that applied through the program diminishes from 30% to 20% of a business workforce (outside of agriculture, construction and healthcare), labour issues could come back fast and add additional pressure of wages.

Inflation is slowing, will wages follow?

For the time being, wage adjustments remain above the historical average. They could reach 3.5% growth in 2024. The vast majority of companies report that they still have to take the high cost of living into account when setting wages.

While inflation is slowing, interest rates remain high and continue to have a large impact on household budgets. Many people will continue to see their purchasing power diminish, even if the speed of price increases slows and the Bank of Canada's key interest rate remains stable.

As a result, wage growth will slow somewhat, but while inflation remains above target and interest rates high, companies will be faced with rising labour costs. Indeed, this has been reflected in recent minimum wage increases across the country.

In a nutshell...

- As an employer, you're likely to continue to face pressure for larger-than-desired pay hikes, even as the job market becomes more balanced and competition for workers less intense.

- Efforts to improve labour productivity, keep up with wage pressures and ensure the successful integration of newcomers into the labour market will be essential to the stability of Canada's labour market.

- The job market is constantly changing, and the workforce will remain a key issue in the coming years. A strategic plan for managing your human resources is essential to ensure the growth of your business and the loyalty of your staff.

- BDC offers you a wide range of tools to help you manage your workforce challenges.

Recession fears ease further

The Bank of Canada recently revised upwards its growth forecast for Canada to 1.5% for 2024, compared with the 0.8% it was anticipating at the start of the year. The main reason for this revision is immigration-supported population growth, which has more than offset persistent weakness in productivity growth this year.

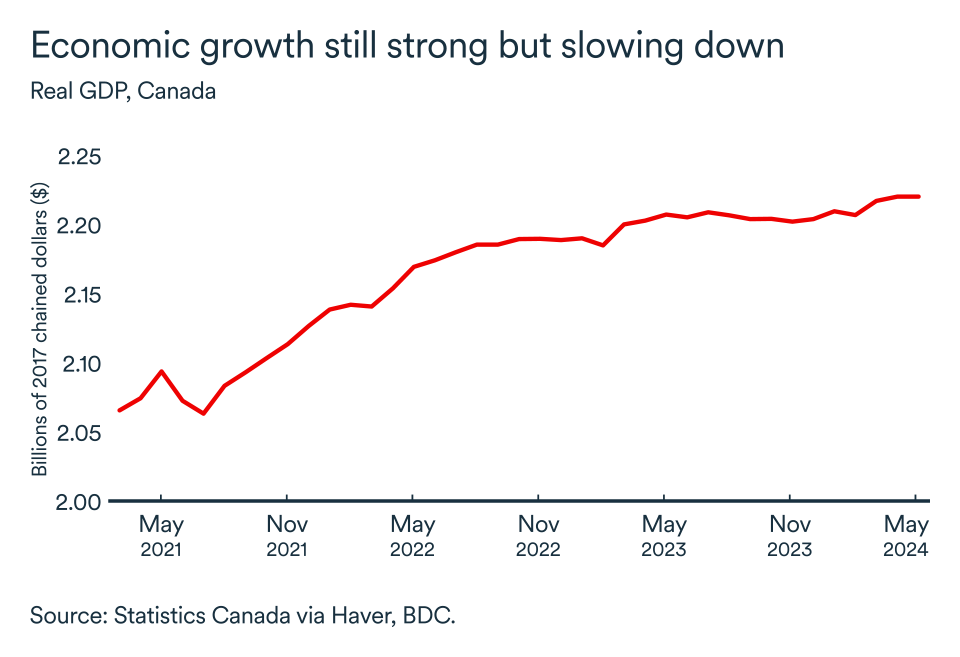

Canada remains on track for a soft economic landing. Real gross domestic product (GDP) rose by 0.2% in February, following a 0.5% increase in January.

Service-producing industries (+0.2%) led growth for a second consecutive month. However, Statistics Canada is forecasting neutral growth in March, based on preliminary data, which would bring annualized first quarter growth to 2.4%. On an annual basis, however, growth for the first three months of 2024 would be 0.7% compared with the same period last year, a sign that the economy continues to decelerate.

Inflation nears target

It's not just economic activity that's slowing but also inflation. Tight monetary policy continues to have the desired effect on the economy. Demand appears to be slowing at an adequate pace to dampen inflation.

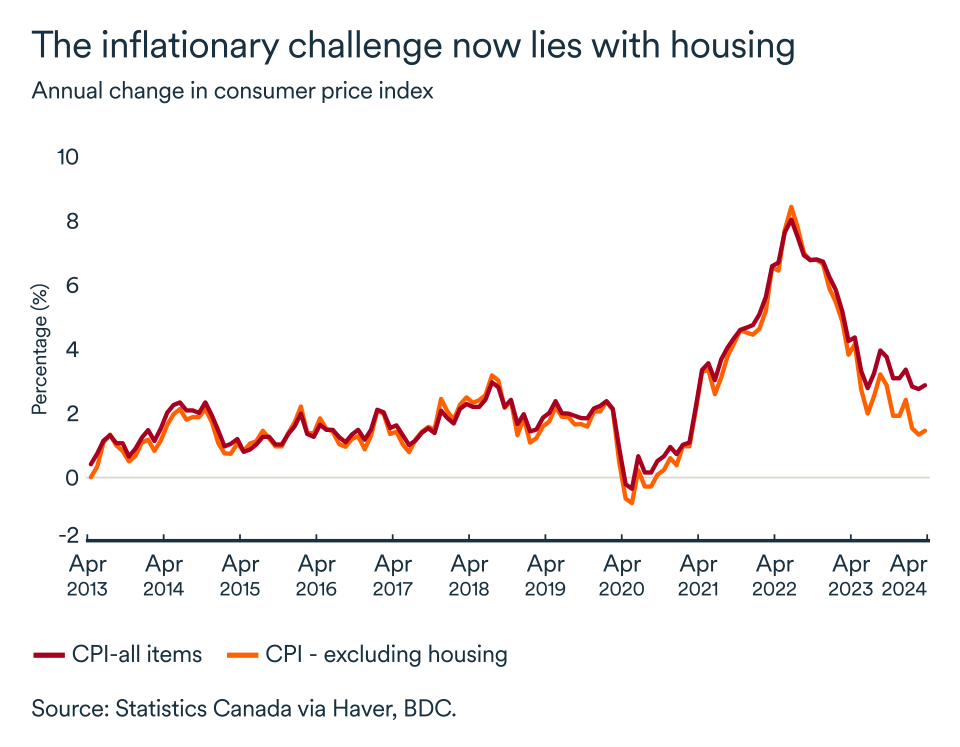

The Bank of Canada's preferred measures of core inflation fell for the third month in a row in March. One of these measures—median inflation—came in below 3%. That was inside the target range for the first time in two and a half years.

This suggests that the bank may be more inclined to cut interest rates at its next meeting in early June, even though headline inflation as represented by the Consumer Price Index has risen slightly. Year-on-year, total CPI rose from 2.8% to 2.9% between February and March.

The rise in core inflation is now essentially linked to housing. In 2024, if we exclude mortgage interest costs, inflation has held steady at 2%. However, decision-makers at the Bank of Canada may continue to exercise caution and, above all, patience when announcing their next rate decision in June, given rising inflation seen in our neighbour to the south. The bank’s Board of Governors may want to see more data and decide to wait until July before making their long-awaited first rate cut.

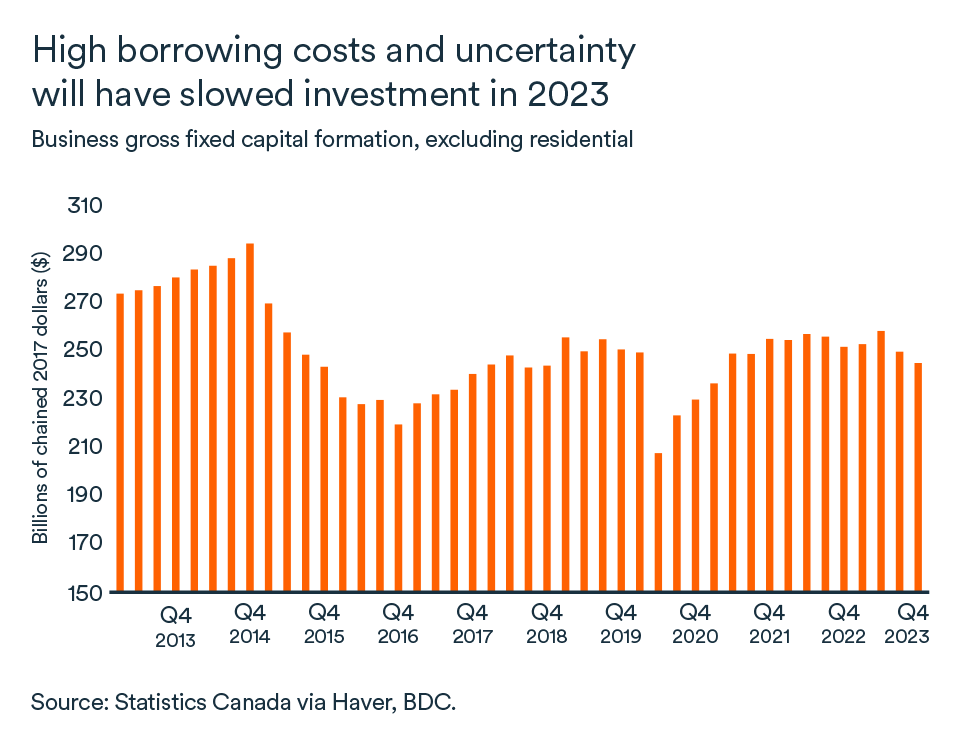

Uncertainty hampered business investment

Of course, high interest rates not only dampen consumer demand, they also curb business investment. Until recently, Canadians feared the economy would slide into recession and consumers have become more cautious in their spending. As a result, companies were faced with uncertainty about the outlook for demand for their products and services and many postponed investment decisions.

Business investment contracted in the latter part of last year. Financing conditions are still difficult for Canadian companies, but they should benefit from lower rates in the second half of the year. The latest report from the Canadian Federation of Independent Business indicates that borrowing costs are an issue for almost half the companies surveyed.

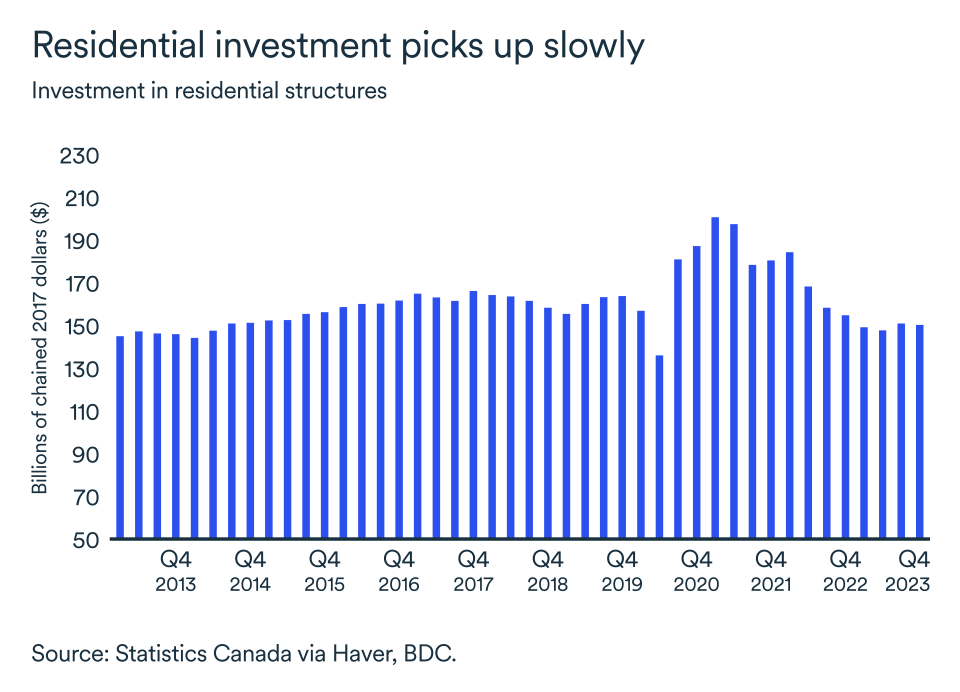

Residential investment should help growth

Last year's 10%-plus contraction in residential investment is unlikely to be repeated in 2024, as the impact of past interest rate hikes dissipates, and the Bank of Canada appears headed for its first rate cut this summer. Builders should regain confidence to invest as prices stabilize in some markets and rise in others.

Population growth means that more people are looking for housing, yet there aren't enough homes available. The federal government aims to increase the supply of housing by a total of 3.9 million units by 2031 and has announced a series of measures to achieve this goal.

Obviously, it will take time before these interventions have an impact on the Canadian housing market. In the short term, we expect housing starts to grow at a steady pace, although a decline was recorded nationally in March compared with February.

The impact on your business

- The Bank of Canada is expected to lower its key rate by mid-July, which should offset some of the slow down making its way through the economy. In the meantime, consumers will remain more cautious, and companies will want to reduce their inventories. It will be some time before your order book is replenished.

- In anticipation of lower interest rates, credit conditions already started to ease and should get even softer once the Bank of Canada starts to lower its policy rate. This is a good time to review your investment projects and prepare for future growth.

- As the housing market adjusts to various policy changes, sectors such as construction, building materials wholesalers and retailers, maintenance and furnishing companies should rebound in the near future.

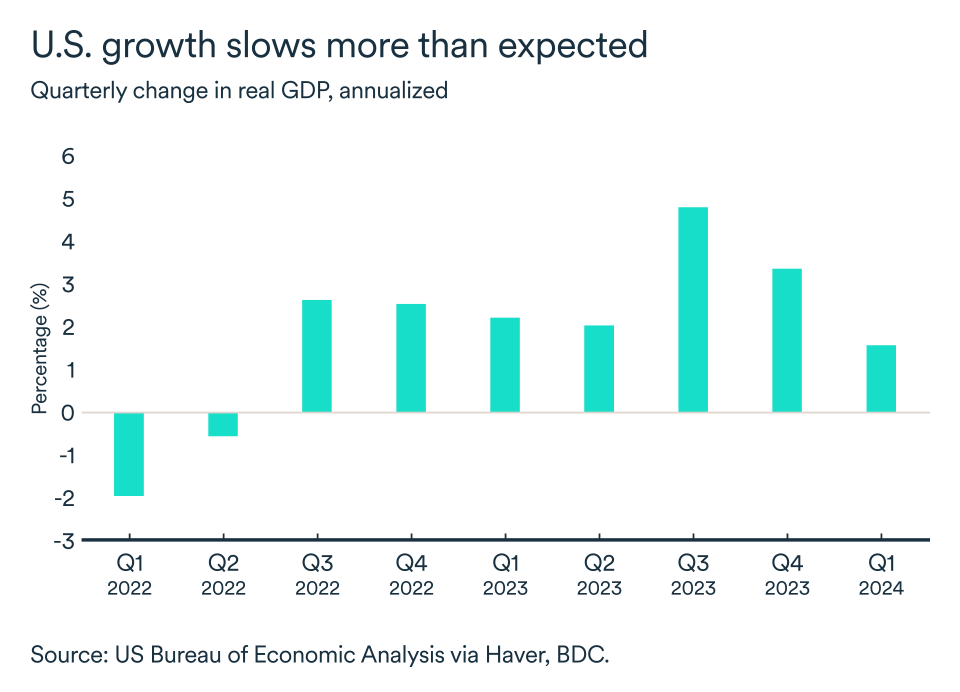

U.S. growth slows but inflation remains above target

The U.S. economy grew by 1.6% in the first quarter, according to preliminary estimates. Although the overall results are still positive, they surprised many observers who were expecting much stronger growth for the start of the year.

Despite high interest rates, the bulk of growth continues to come from households. Consumption and residential investment saw the biggest gains in the first three months of 2024.

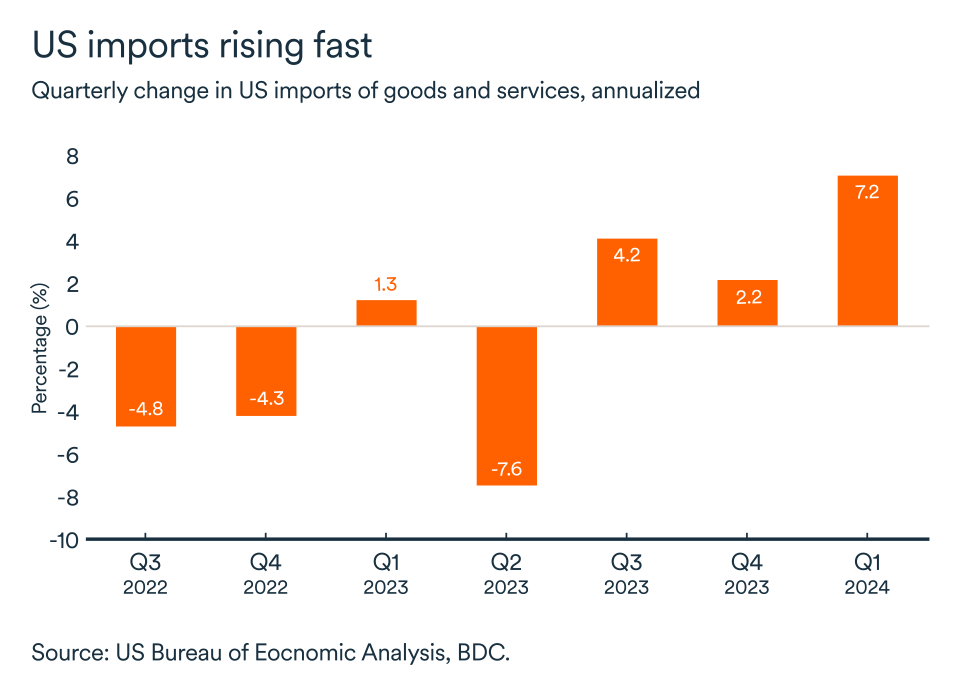

Exports also increased, but not enough to offset an acceleration in imports (which are deducted from gross domestic product).

Interest rates unchanged

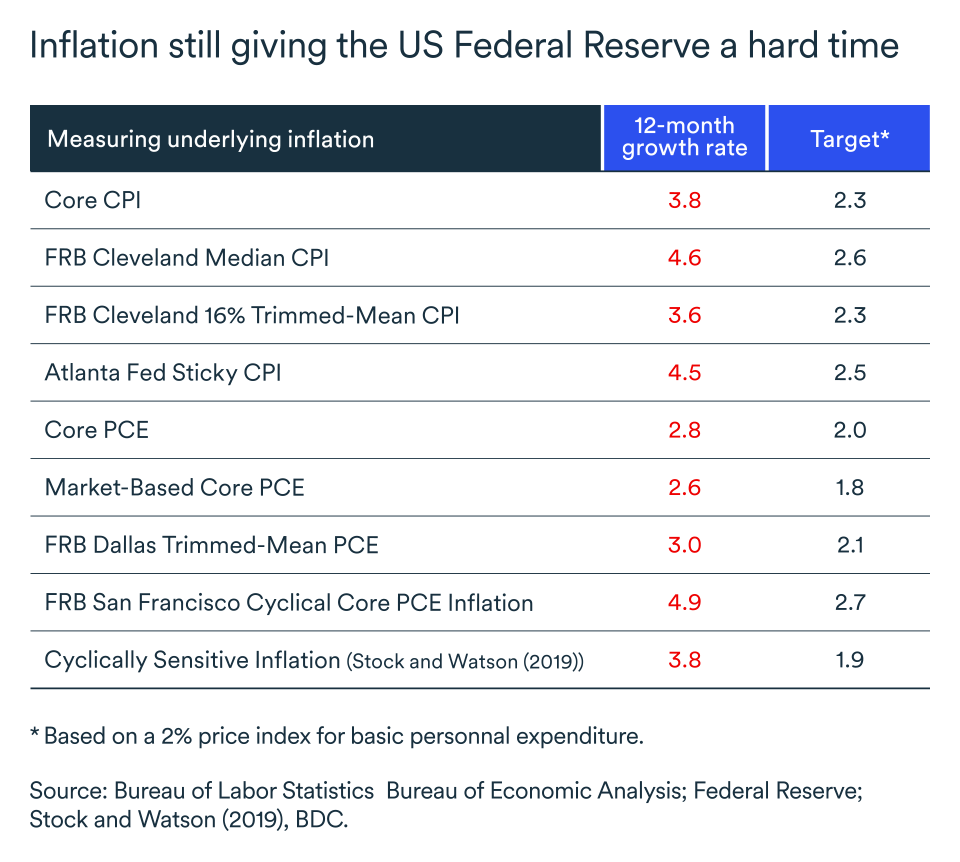

As expected, the Federal Reserve maintained its key interest rate at 5.25-5.50% at the beginning of May, given that inflation remains above its 2% target and the labour market is still solid.

If future inflation data show better progress, the Fed should be able to cut interest rates later in the year. Core inflation in the personal consumption expenditure index was 2.8% in March while core inflation in the consumer price index was 3.8%. To reach the Fed’s target, which is a reading in the core personal consumption expenditure index of 2%, the core consumer price index (CPI) would have to reach 2.3%.

Therefore, these inflation measures are still too high for the Fed to cut rates anytime soon. Notwithstanding the acceleration in inflation during the quarter, U.S. economic activity came in at a pace slightly below what Fed officials consider to be non-inflationary (1.8%). So, we'll probably have to wait until autumn at the earliest before U.S. interest rates finally begin to descend.

Employment growth still solid but also slowing

The job market is strong but has weakened in response to cooling demand in the economy. The rate of job quits and new hires have virtually returned to pre-pandemic levels. The creation of 175,000 new jobs in April was a good performance but less vigorous than in the first quarter. The national unemployment rate edged up to 3.9% last month, which is still historically low, although slightly higher than levels prevailing at the same time last year.

Wages rose at a year-on-year rate of 3.9% in April, slightly faster than the general price level. The good news is that, given the stability of interest rates and the positive effect of rising real wages (i.e. net of inflation), household spending should hold up well over the coming months, supporting overall economic growth without necessarily increasing pressure on inflation.

Will American households start tightening their belts?

While the labour market only started showing signs of weakening in April, consumer goods spending slowed in the first quarter. Indeed, growth in goods consumption was negative for the first time since the summer of 2022. Therefore, what growth there was came in spending on services, which is less sensitive to interest rates.

However, the strength of the U.S. dollar encourage consumption of goods made elsewhere. U.S. imports surged by 7.2% in the first three months of the year.

The impact on your business

- Tight monetary policy is increasingly weighing on domestic demand, but the Federal Reserve was still not convinced that the time was ripe for a rate cut at its May meeting. The U.S. economy should therefore continue to slow over the coming months.

- Canadian companies exporting consumer goods to the U.S. should continue to benefit from a favourable Canada-U.S. exchange rate. Cash-strapped U.S. consumers can get a good discount from buying in Canada.

- U.S. companies have invested more in software and R&D in recent months, boosting their productivity. Canadian entrepreneurs should follow suit if they want to stay competitive.

The oil market navigates shifting tides

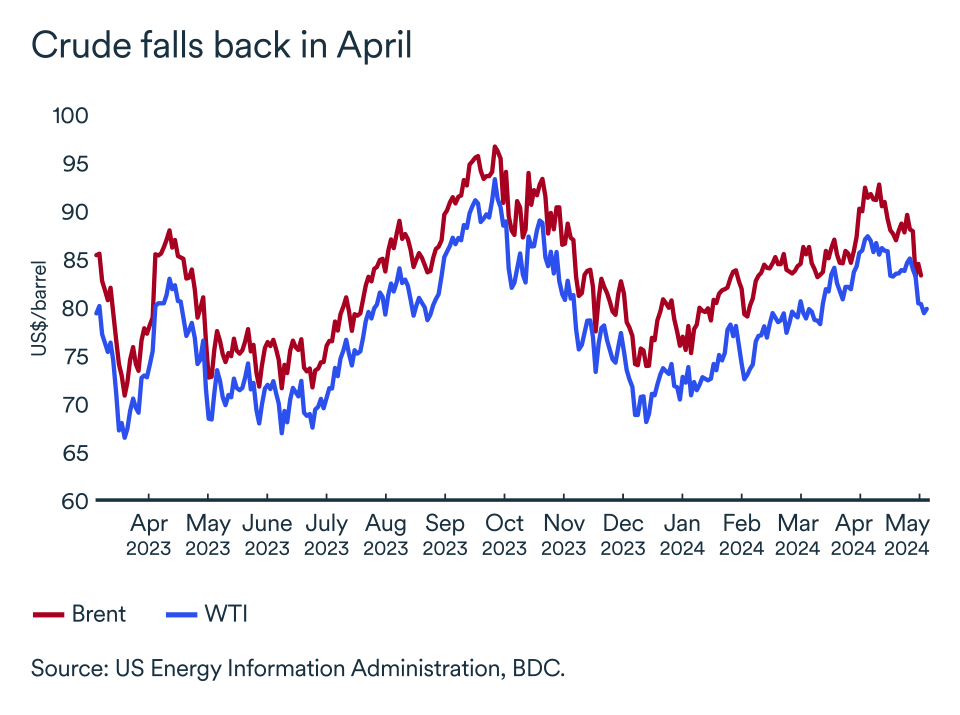

World oil benchmarks fell by almost 10% between the beginning of April and May. Brent crude was trading at around US$83 a barrel, and WTI at US$78. Part of the reason for this decline was the easing of fears that an escalation of hostilities in the Middle East would affect oil supplies. The oil market has experienced significant fluctuations in 2024 as the situation in the Middle East evolved rapidly.

Risk persists in the Middle East

The geopolitical situation in the Middle East will remain at the forefront of oil market concerns, and crude prices will move in step with the situation. Uncertainty over the future direction of crude prices could pose a significant challenge to the Organization of the Petroleum Exporting Countries and their allies (OPEC+). The organization's ministers will meet on June 11 to set oil production targets for the following three months.

OPEC+ is expected to extend production cuts in June, as stable inventories and the most recent price decline suggest a balanced market. However, OPEC+ may be tempted to reverse some earlier cuts to avoid losing market share to non-OPEC producers. Some member countries have long argued in favour of raising the base production level.

In fact, the United Arab Emirates recently announced an increase in its oil production capacity to 4.85 million barrels per day (Mb/d), from 4.65 Mb/d at the end of 2023. With current production of around 3.2 Mb/d, the UAE has substantial spare capacity, equivalent to around 1.8% of the world's total crude supply.

U.S. demand is also a factor

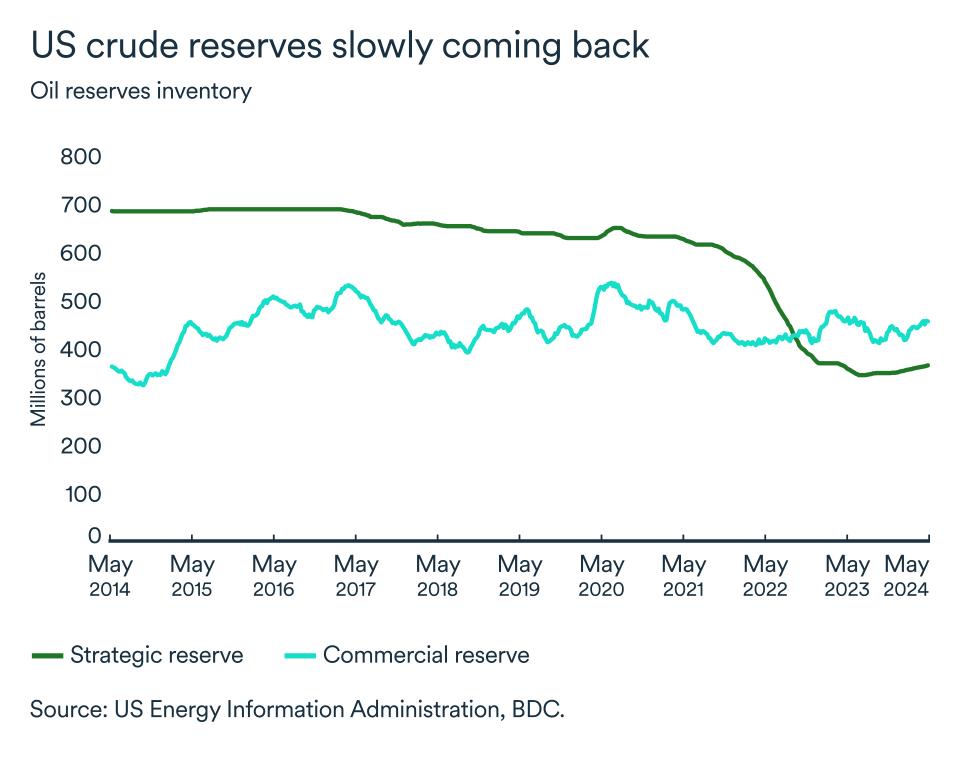

Oil prices were also affected by concerns over the outlook for oil demand in the United States. Weaker-than-expected growth in the first quarter was accompanied by an unexpected rise in U.S. commercial crude inventories.

Growth in U.S. oil demand is likely to be relatively moderate over the next few months, due to high interest rates in the short term and improved vehicle efficiency in the medium term. American authorities are also prepared to intervene in the crude oil market to offset potential variations associated with the Middle East risk premium.

Discussions have already resumed on the possibility of using strategic oil reserves to lower retail fuel prices in the event of escalating conflict between Israel and Hamas.

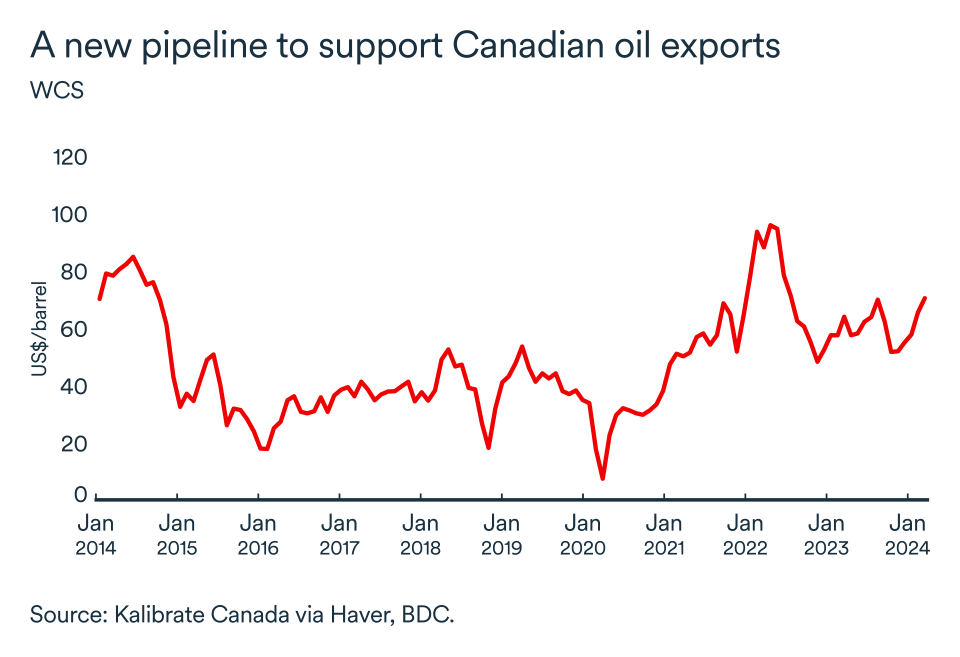

New export opportunities for Canadian oil

In Canada, the Trans Mountain Pipeline expansion project went into service after more than 12 years of construction. The pipeline has been filling with oil since May 1. The expansion almost triples the shipping capacity of the Trans Mountain system from 300,000 barrels per day to 890,000 barrels per day.

The pipeline should help reduce the differential between American (WTI) and Canadian (WCS) oil prices. The increased pipeline capacity will help open up global export markets for Canadian oil, particularly to Asia. According to the latest information, tankers will be able to load at the Westridge Marine Terminal in the Port of Vancouver by mid-May.

In a nutshell...

The tightening of oil supply and depletion of stocks widely anticipated at the start of the year have yet to materialize. The major fluctuations in the oil market are essentially due to changes in tensions in the Middle East. Crude prices, therefore, will remain at risk of rapid fluctuation as events in the conflict unfold.

Despite this, there has been no real impact on oil supplies since the start of the war, and the risk premium has largely faded. In North America, U.S. oil inventories are rising as demand slows. U.S. authorities say they are ready to dip into their strategic reserves once again to supply the market in the event of prices getting too high. Meanwhile, the commissioning of the Trans Mountain Pipeline expansion will enable Canada to significantly increase oil transport to new markets.

Slower growth could lead to rate cuts this summer

Canadian economic activity is slowing. After the 0.5% and 0.2% rises in GDP in the first two months of 2024, growth in March was forecasted to have remained flat. The Bank of Canada’s higher interest rates seem to be working their way through the economy. We reiterate that we expect the Bank of Canada to start lowering rates by mid-July, bringing them down to 4.25% or 4% by year-end.

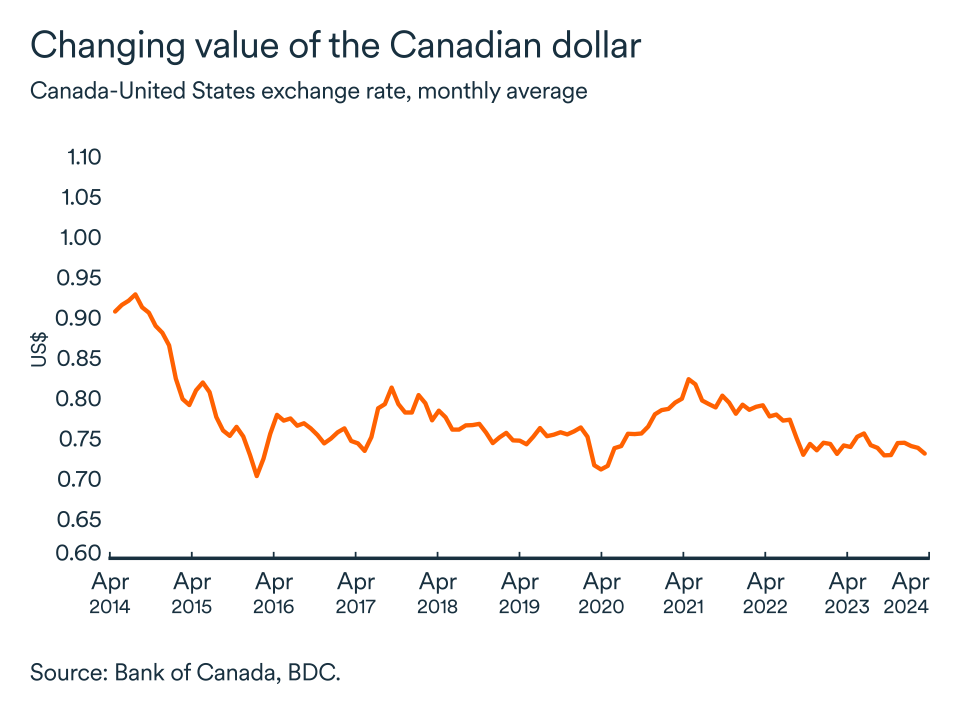

The loonie weakens in April

The Canadian dollar weakened in April, averaging US$0.73, a hundred basis points lower than the previous month. The U.S. dollar has appreciated since the start of the year, reflecting the strength of the U.S. economy as well as rate cut expectations being pushed back further.

The U.S. dollar will remain strong in the current context, which will further support the competitiveness of Canadian exports. We expect the exchange rate to fluctuate between US$0.72 and US$0.75.

Sharp drop in confidence this month

The CFIB's confidence index for the year ahead dropped in April. Optimism decreased from 52.7 to 47.5 between March and April. A minimum wage increase on April 1 in many provinces put pressure on small businesses that are feeling the pinch of higher interest rates more than larger businesses.

Confidence varied among provinces. While most provinces remain optimistic, two of the largest, Quebec and Ontario, registered levels below the 50 mark.