Monthly Economic Letter

Keep abreast of key economic indicators.

Read moreYou have questions, we have answers!

As we enter the new year, one word describes the economic environment: uncertainty. To help you see things a little more clearly, this edition of the Economic Letter answers the 10 questions most frequently asked of BDC economists.

1. What can we expect for the Canadian economy in 2025?

Despite all the uncertainty, interest rate cuts have improved household and business confidence, which bodes well for the economy as a whole. We forecast economic growth, as measured by real GDP, to reach 1.5% in 2025, a modest acceleration from 2024.

However, entrepreneurs will have to be patient because the economic recovery will be gradual. As some of the risks currently facing Canada dissipate, the economy should gain momentum. Full economic recovery will therefore take some months. So make sure your company is ready to weather short-term turbulence while preparing to take full advantage of stronger growth ahead.

2. What's the outlook for inflation and input costs?

Rising costs and inflation were the main challenges for businesses in 2024 and there's good news on that front. Inflation should remain within the Bank of Canada's target range of around 2% next year. However, inflation could be higher for services, which are strongly linked to wages, as well as for housing prices.

By contrast, prices for many raw materials could fall in 2025. This is likely to be the case for oil and some metals as growth in global manufacturing activity is expected to remain modest, particularly in China. More supply-constrained resources, such as natural gas and some fertilizers, are likely to see price increases in 2025 while demand for precious metals is rising due high uncertainty. Most of the price gains in these markets occurred in 2024, but prices are likely to remain high over the course of this year.

Overall, an aging population, the energy transition and global geopolitical risks will continue to exert upward cost pressures for businesses. These challenges will persist beyond 2025, which is why it’s vital for companies to boost their profitability and productivity to adapt to this new business environment.

3. Should we opt for fixed or variable interest rates?

The Bank of Canada’s policy rate, which sets the trend for interest rates, has fallen from 5.0% to 3.25% in just six months. We expect it to drop to 2.5% by the end of 2025. So, in general, rates look to be on a downward trend this year.

Variable rate loans benefit quickly from Bank of Canada rate cuts, but fixed-rate loans move slower because they are guided more by developments in the bond market where future rate cuts have already been priced in. Since June 2024, the Bank of Canada’s policy rate has fallen by 175 basis points, but five-year bond yields have dropped by just 45 points.

In choosing between fixed and variable financing, there are many factors to consider besides rate expectations. The decision also depends, among other things, on the duration of the loan, its structure and conditions, your ability to repay including anticipated income variations and, of course, your appetite for risk.

4. Will consumer spending return this year?

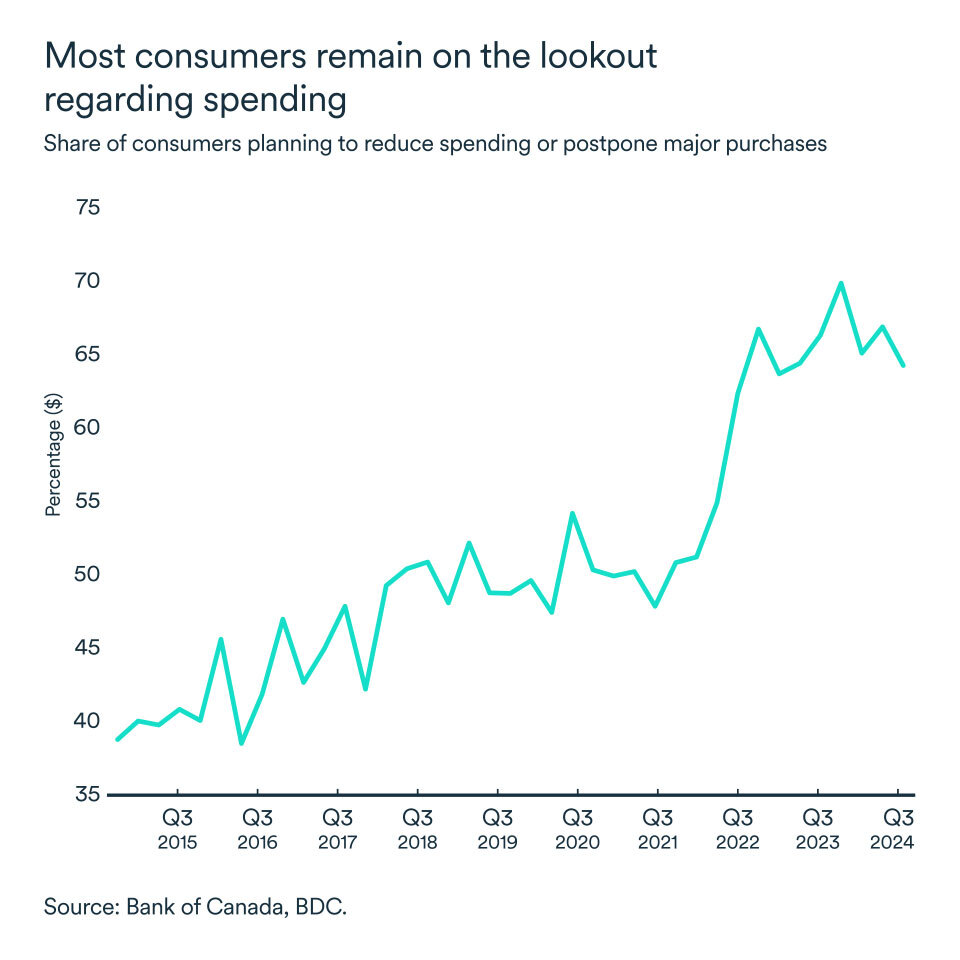

The good news for businesses is that consumer spending in Canada should continue to rise this year. While lower interest rates began to have a positive impact on the real economy at the end of 2024, the gains so far have been modest in terms of discretionary consumer spending. This is because, for the time being, effective interest rates for households remain high, despite the significant reductions implemented by the Bank of Canada last year.

Canadian households have been able to maintain their savings rate at a high level, while modestly increasing the pace of consumption thanks to a nearly 10% increase in disposable income by the end of 2024. This bodes well for continued growth in consumer spending in the months ahead. Surveys indicate that perceptions of financial stress have improved. With recent interest rate cuts and lower inflation, fewer consumers expect to have to cut back on spending. But they remain vigilant as high debt levels continue to weigh on Canadian households.

We shouldn't expect a sharp rebound in spending but rather a steady improvement in the months ahead.

5. Will unemployment continue to rise?

Employment gains stagnated at the end of 2024 (except for December big bump), causing the unemployment rate to rise and the pool of available labour to increase. The Canadian economy created around 413,000 jobs in 2024, but many more potential workers joined the workforce. That sent the unemployment rate as high as 6.7% at year-end.

Given the level of economic uncertainty, we expect companies to favour maintaining their current workforce rather than increasing it substantially.

However, the slowdown in immigration, combined with the retirement of baby boomers, should curb the rise in unemployment. We also don't expect major layoffs. Instead, departing workers will not be systematically replaced. Thus, job vacancies in the country should continue to decline.

6. What will happen to wages in this context?

Now that inflation has eased considerably, wage growth has been rising faster than prices on average. We expect wage expectations to moderate this year compared to recent years. Even so, private-sector wage growth is forecast at 3.5%. For employers, holding on to the best workers remains at the heart of an effective HR strategy. If you’re not able to compete on salaries and overall compensation, keep in mind that corporate culture and innovation are also important factors in employee retention.

7. How low can the loonie go?

The Canadian dollar continues its gentle downward slide. The loonie, which was trading at US75 cents a year ago, started the year below 70 cents, a low not seen in almost five years at the start of the pandemic.

Much of the dollar's losses against the U.S. dollar reflect the difference in the economic fortunes of the two countries in 2024 and a resulting interest rate differential between the U.S. Federal Reserve and the Bank of Canada.

The difference in the monetary policy stances is set to continue into 2025 and may even grow. The threat of tariffs is also having a major impact on the loonie's value against the greenback. The Canadian dollar should remain between US$0.70 and US$0.72 in 2025 but could slide below this if trade tensions grow.

In general, the impact of the Canadian dollar's value depends on the nature of your business and its dependence on imports versus exports. A weak Canadian dollar supports exports. If, on the other hand, you are importing inputs or machinery, your operating costs could rise in the coming months.

8. Will the housing market stabilize?

The Canadian housing market is the most rate sensitive sector. Just as higher rates rapidly dampened the volume of real estate transactions and prices, the market has reacted strongly and quickly to interest rate cuts. Home sales have jumped 18.4% since May 2024, just before the first rate cut was announced.

With the accumulation of rate cuts, combined with an easing of mortgage rules, the market will be increasingly active this year. In this context, it wouldn’t be surprising to see several regional markets begin to overheat once again.

9. How will demographic changes affect the economy?

It's no secret Canada's population is aging. In recent years, population growth has come almost entirely from immigration. The reduction in immigration targets for 2025-26 will lead to a modest decrease in the population. As a result, the labour market could once again become tighter with the reduction in the pool of available workers. Beyond the impact on the job market, the aging of the population also means changing needs and consumption habits.

The country’s changing demography holds both risks and opportunities for small and medium-sized businesses. You should work to position your business to meet current demographic trends and sustain growth. One way to tackle the challenge is to adopt a generational approach to identifying consumer trends affecting your customers.

It’s also important to ensure there’s an ongoing transfer of knowledge from your company's more experienced employees to younger ones to support effective succession.

10. How to cope with all this uncertainty?

The immediate reaction to uncertainty is often to go into hibernation and adopt a “wait and see mode”. This uncertain time should be seen as an opportunity to reinvent yourself and improve your business. Understand the changing needs and expectations of your clients, rebuild your cost structure for the new reality, embrace digital technologies, review your HR needs and real estate assets, but most importantly, show strong leadership through the whole process.

Our article on how to thrive in difficult times gives you a number of tips on how to cope in uncertain times.

The 2-minute essentials

An uncertain start to the year for the Canadian economy

At the start of the new year, Canadian consumers appear worried about their job prospects, future financial situation, real estate values and the economy in general. All regions experienced a deterioration in consumer sentiment in these areas, according to the latest Bloomberg Nanos consumer confidence report.

After a brightening of consumers’ mood in late 2024, the report shows that pessimism regained ground over the past two months as expectations for the future strength of the economy hit a two-year low. Optimism will have to pick up before the economy can fully benefit from the expected momentum from a series of interest rate cuts.

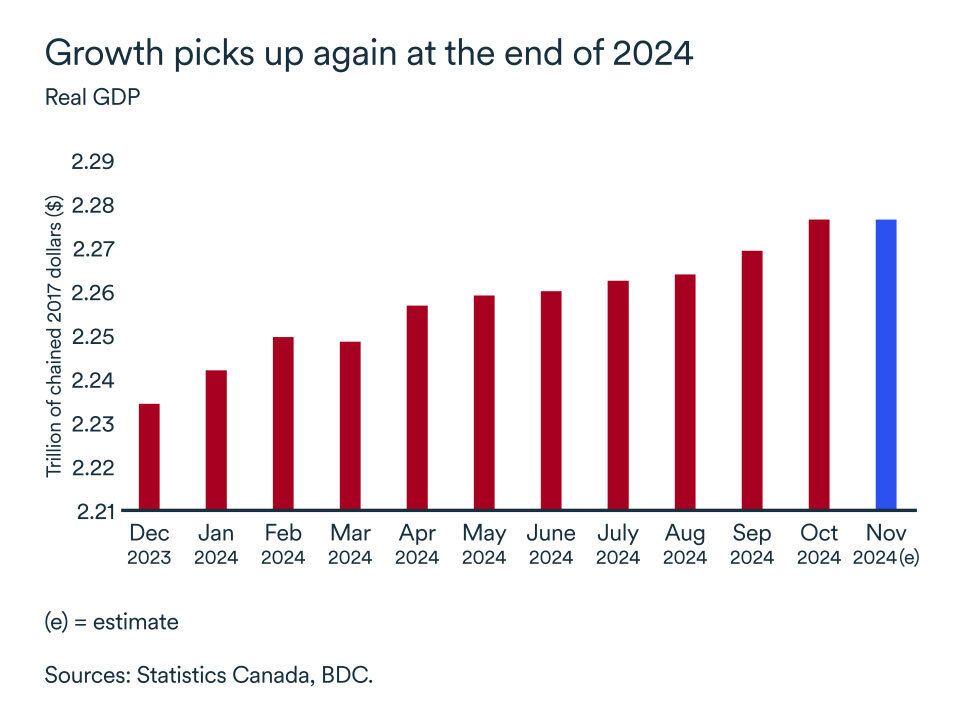

Growth rebounded late in 2024

The economy grew by 1.4% between January and October 2024, mainly due to service industries. In October, gross domestic product (GDP) rebounded (+0.3) from September. The goods sector posted an increase (+0.9%) after four months of decline. The services sector, which accounts for some 70% of the Canadian economy, continued to grow (+0.1%) compared to the previous month, thanks to strength in the real estate sector.

Growth was largely due to oil and gas extraction. However, according to Statistics Canada's preliminary estimates, GDP fell by 0.1% in November. If this is confirmed, economic growth came in at 1.3% for the first 11 months of 2024.

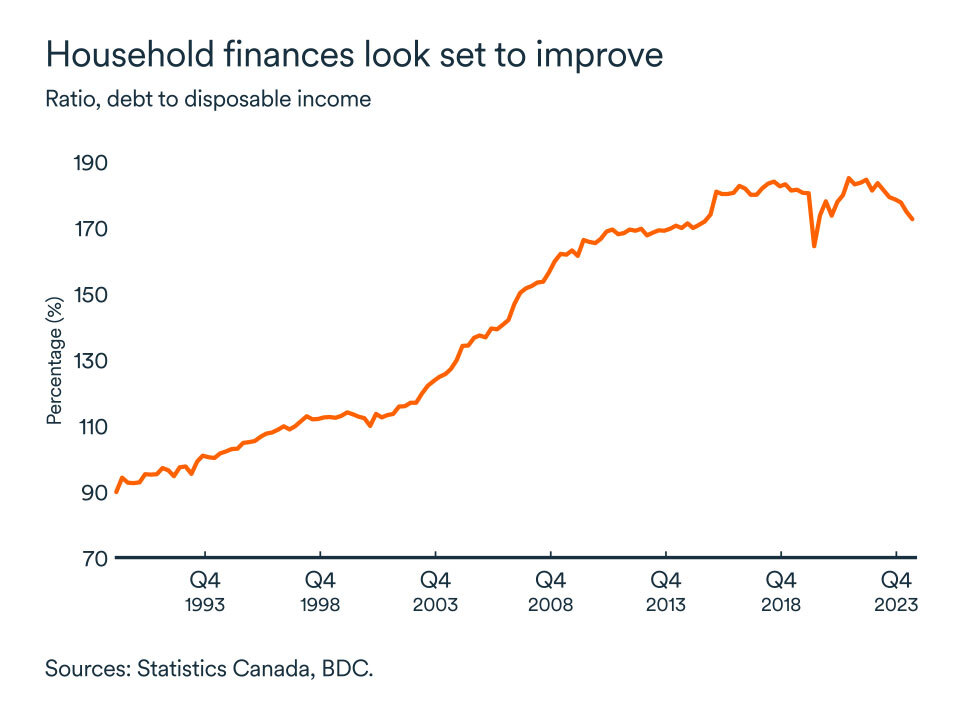

Total household debt increases, but disposable income rises faster

In the third quarter of 2024, household debt on the national balance sheet reached $3 trillion. However, at the same time, disposable income rose by 2%, sending the ratio of household debt-to-disposable income lower for a sixth consecutive quarter. Excluding distortions due to the pandemic, this is the lowest ratio since 2015. Debt repayments increased by 0.2%.

Despite a decline in real estate values resulting from higher interest rates, household net wealth continued its upward trend of the past two years, supported by strong financial markets. The wealth effect could be a key factor supporting stronger consumer spending in 2025, particularly as house prices are expected to rise.

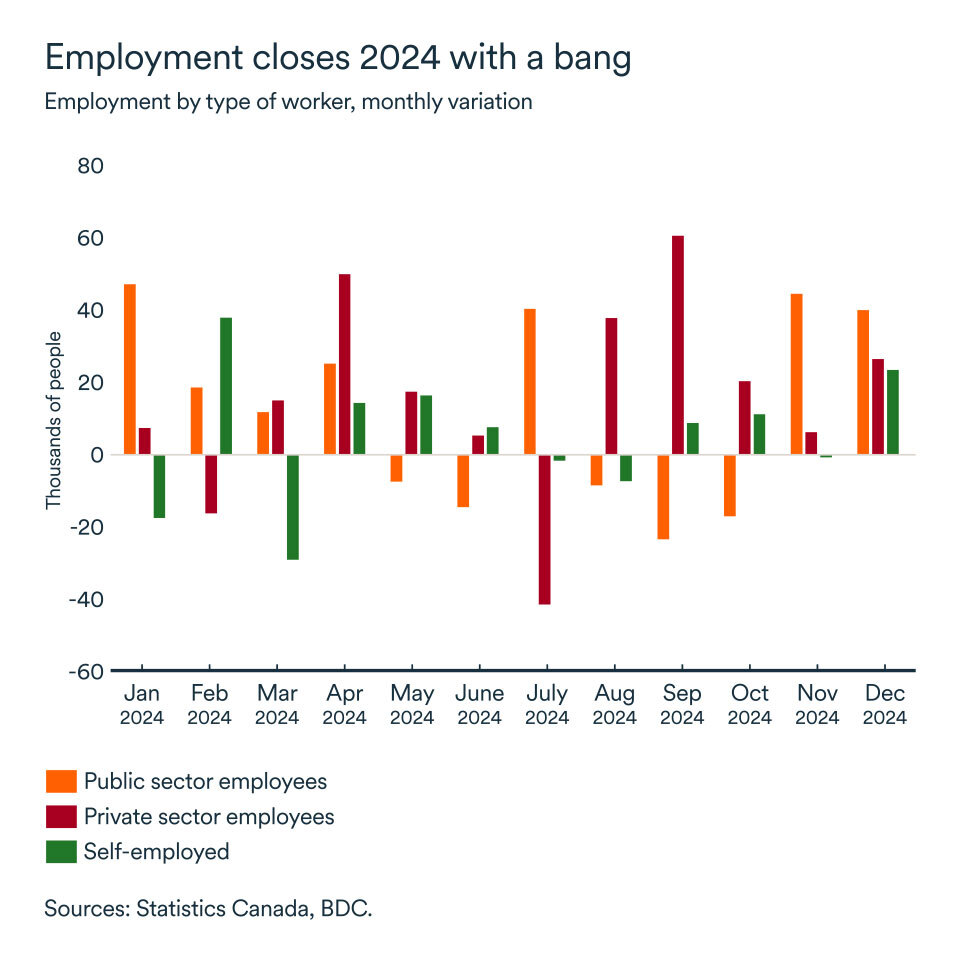

Employment ends the year on a high note

Job creation closed 2024 strongly with the addition of 91,000 jobs in December. In total, the Canadian economy created 413,000 jobs in 2024. At 6.7%, the unemployment rate is slightly lower than the level it reached in November but remains among the highest recorded in the country since 2017 (with the exception of the pandemic period).

Once again, job creation in December was concentrated in the public sector, while the number of private-sector jobs picked up in December, it stagnated in the fourth quarter overall. This shows once again that companies remain cautious in hiring despite interest rate cuts, reflecting the slow recovery of demand in the economy amid heightened uncertainty.

The unemployment rate fell in Alberta, Ontario, Quebec and Newfoundland and Labrador and rose in the other provinces.

The impact on your business

- Early indicators suggest that Canada returned to a pace of growth approaching potential in the final quarter of 2024 at just under 2.0%. But uncertainty will limit a pickup in momentum that might have been expected given the significant rate cuts by the Bank of Canada.

- The financial picture of Canadian households along with lower interest rates, controlled inflation and a still-robust labour market provide a solid foundation for a recovery in consumer spending in 2025. However, uncertainty over tariffs and other issues is hurting confidence and it will likely take time for the economy to benefit fully from these catalysts.

- Many companies are showing caution in hiring, inventory management, spending and investment. If your business has this mindset, make sure you’re also preparing for a return to growth because the economy remains on a solid footing.

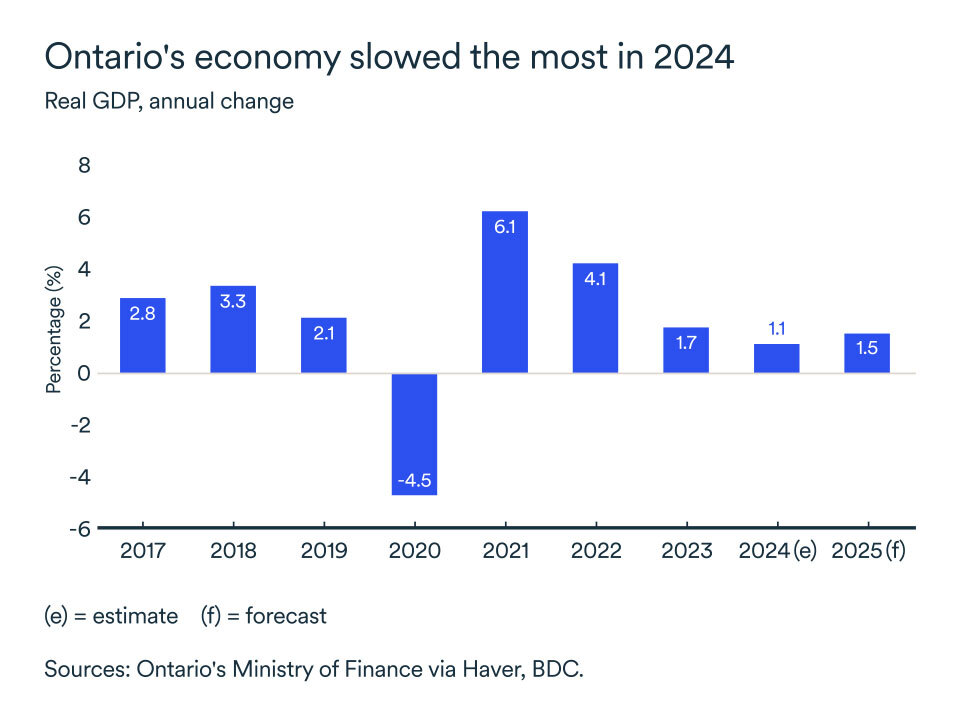

Ontario’s economic growth expected to pick up in 2025

After two years of rising interest rates, the effects on Ontario’s economy were fully felt in 2024. High rates dragged down consumer spending, the housing market and business investment. The result was the most marked slowdown among the provinces last year. In 2025, we should see a slow rebound. Rate cuts will start working their way through the economy and growth will improve, especially in interest rate sensitive sectors. The residential housing market will be an important driver of growth and further support will come from major investments in the auto sector

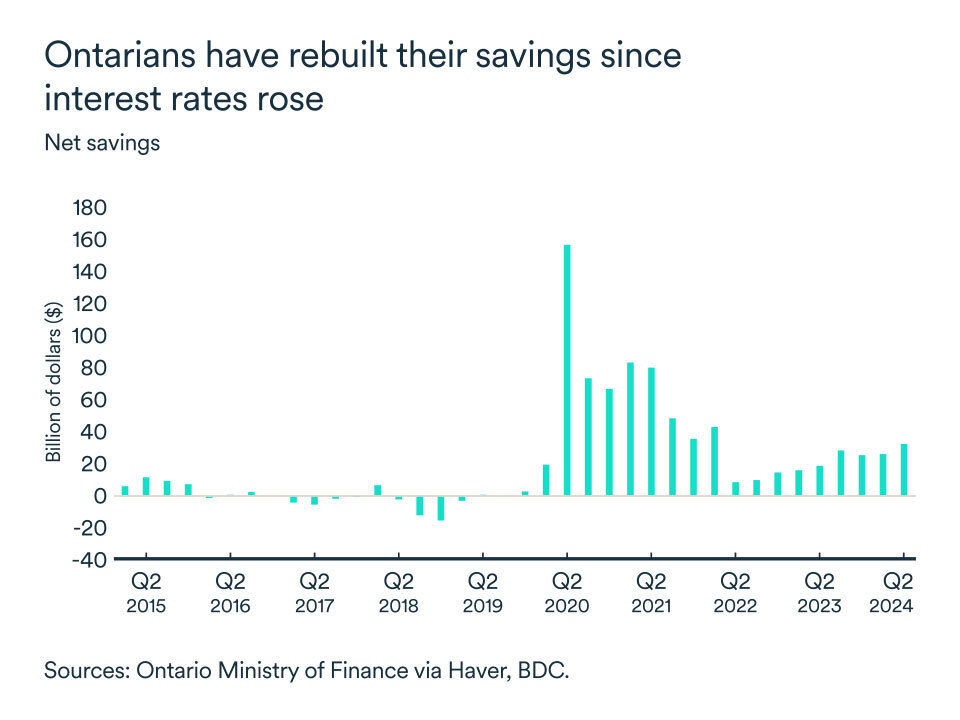

Higher mortgage payments will hurt, but overall household spending should increase

Since 2022, household spending in Ontario has been cautious in the face of higher debt payments. When the Bank of Canada began increasing rates in the first quarter of 2022, Ontarians turned to rebuilding their savings.

This year, homeowners renewing their mortgages will still have to do so at higher rates despite last year’s reductions. This will push them to save more and limit their spending. However, many households are either mortgage-free or are not facing a renewal this year.

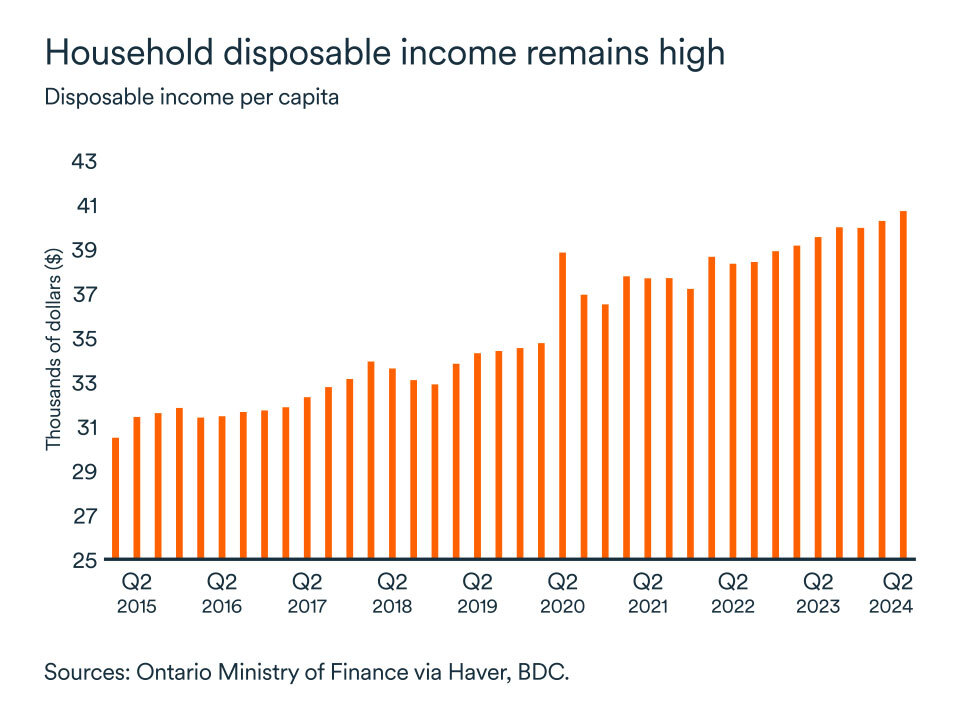

Overall, higher disposable income per capita, lower rates and the Ontario’s government’s family rebate policy, coupled with some possible federal tax relief, should lead to stronger consumer spending this year and a return to the long-term growth trend in consumption

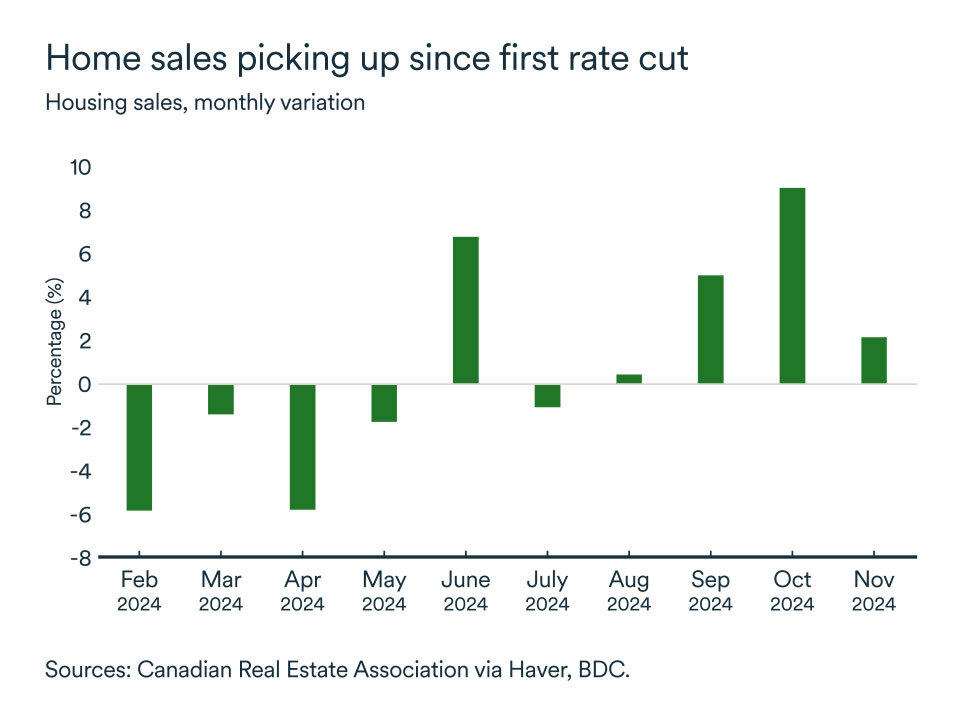

Housing market recovers

The skies are finally clearing for the housing sector in Ontario. Home sales began rising quickly after the Bank of Canada kicked off its rate cutting cycle in June 2024. While we don’t expect a return to peak levels in the real estate market due to an expected population decline in the next two years, we still think the market will perform better in 2025. However, lower population growth will likely impact demand for rentals and dampen investor appetite keeping a lid on price increases.

On the residential investment side, the Bank of Canada will continue to lower rates this year and the government plan to build 1.5 million homes by 2031. These factors should stimulate residential construction this year and beyond. Longer term, residential development should be supported by a return to population growth once temporary measures on immigration are lifted.

A slow start to the year should give way to stronger growth

At the start of 2025, sectors that struggled in 2024 continue to deal with uncertainty generated by the threat of trade tariffs. Last year, a weak housing market weighed on the construction sector and weaker demand for goods hurt the manufacturing sector. Manufacturing sales declined by 5.4% at year end, dragged down by a decline of 7.9% in durable goods sales and retooling of plants in the Ontario and the U.S.

However, consumers are expected to spend more on goods in 2025 which should help the manufacturing sector and overall growth. For exporters, U.S. demand for Ontario’s goods should remain positive as long as tariffs threats are not fully implemented. Despite headwinds, the outlook for the province is positive with major projects in the works. Honda announced a massive $15-billion investment in four new electric vehicle battery and assembly plants. Another $2 billion is being invested to refurbish a nuclear energy plant to meet growing clean energy demand. These projects in the non-residential sector are important for the province and will feed through the economy this year and following ones.

The impact on your business

- Lower interest rates will lighten consumer debt burdens, freeing up cash for spending. This could present opportunities for your business to improve sales by targeting specific markets.

- Credit conditions are easing for businesses and entrepreneurs will have access to financing at lower cost. A good way to start the new year is by planning your future investments with an eye to improving your company’s productivity.

- Major investments in certain sectors will have ripple effects through the economy. It’s a good time to assess how your business can take advantage of opportunities in your sector.