Amortization period

The amortization period is the length of time it takes a borrower to pay back the full amount of a loan principal plus the associated cost of borrowing (interest). An amortization period is typically set out in months or years.

The loan principal is paid according to an amortization schedule, typically through equal monthly installments. A portion of each loan payment will go toward the loan principal while the rest will cover interest charges.

For how long should I have my loan amortized?

Your amortization period should be based on two elements:

- the asset being financed

The loan amortization period is normally based on the useful life of the asset. This is done to tie the cost of the asset to the revenues it generates over its useful life. - your cash flow

While it can be tempting to want to pay back a loan as early as possible, doing so risks putting pressure on your cash and could limit your ability to reinvest in your business. Choosing an amortization period that’s too short could also put your business at risk should interest rates start rising.

“If you think about your home, you don’t want to pay your home mortgage back in three years—because the payments would be so high, you’d never be able to afford to live there,” says Nabil Jaffer, Manager, Major Accounts, BDC.

“It can be better to take a longer amortization period and pre-pay the loan if you have extra cash than to lock yourself into an amortization period that reduces your financial flexibility,” points out Jaffer.

It can be better to take a longer amortization period and pre-pay the loan if you have extra cash than to lock yourself into an amortization period that reduces your financial flexibility.

Nabil Jaffer

Manager, Major Accounts, BDC

Why are different loans amortized over different lengths of time?

The amortization period is typically linked to the asset being purchased.

“If banks are financing a piece of real estate, they’d look at amortizing it over 20 or 25 years, but if we are financing a piece of equipment, we usually look at its useful life. If that’s 10 or 12 years, we’d amortize the loan over that amount of time; if its useful life is only five years, we’d amortize it over five years,” explains Jaffer.

A financial institution will do research to define the useful life of the asset.

“Generally, we amortize buildings for 25 years, unless they are quite old, or if they are very specialized in use. As an example, gas stations are generally hard to re-purpose because of all the costs associated with converting the property to another use; those buildings are typically amortized over 20 years.

Amortization example

Some financial institutions, such as BDC, offer borrowers the option of an initial interest-only period. This can be for as long as a year, allowing the borrower to set aside some of the business’s cash before payments on the loan principal begin.

“It could be useful, for example, if you are buying a building, and you might have costs related to moving and renovations. Your payments would be lower because you would be paying interest only for the year, not the principal and interest,” he explains.

Jaffer says the amortization period on loans with a one-year interest-only period would be increased by one year. That means that a loan amortized over 25 years would actually be a 26-year loan.

BDC typically amortizes its working capital loans over a shorter period, Jaffer says, because these loans usually have no tangible security.

Should I pay my loan off more quickly if I have the cash?

Deciding whether to pay off a loan more quickly really depends on your cashflow.

“By paying down your loan more quickly, you may save on some interest costs; but if you are going to have to borrow the funds a year or two down the road you might not have done yourself any favours because you’ll have to go through the whole loan process again,” says Jaffer.

Jaffer adds that if interest rates change, you’ll end up paying a high rate on the new loan. He suggests prioritizing your company’s growth over repaying your loans.

“If you have a really good year or a really good sale and you have excess cash, then you can put a pre-payment on the loan. But if you do that every year and you find you have to keep borrowing on the other end, you are really creating extra work and perhaps extra costs. So, loan pre-payments should really be based on your cash flow. Typically, you can pay off 15% of the loan every year without any penalty,” he says.

Is it important to shop for amortization periods?

The amortization period is one of several factors you should consider when shopping for a loan.

All banks offer different amortization terms. Some lenders may only amortize an equipment loan for up to five or six years, even if the useful life of that equipment is 10 years, whereas other lenders will offer a loan for that same equipment amortized over 10 years.

It’s not just the interest rate you need to look at when you are shopping for a loan, you also want to make sure the amortization schedule works for your business.

Nabil Jaffer

Manager, Major Accounts, BDC

Similarly with real estate, some lenders will cap their loan amortization period at 20 years, but other lenders will offer a 25-year loan amortization period.

“So, it’s not just the interest rate you need to look at when you are shopping for a loan, you also want to make sure the amortization schedule works for your business,” says Jaffer.

Benefits of short- or long-term loan amortizations

- Short-term loan amortization benefits

A short amortization period will allow you to pay less interest overall, but the monthly payments will be higher.

The downside of a shorter amortization is that businesses are often using their cash flow to pay down the loan, which can hinder their ability to invest in other issues. - Long-term loan amortization benefits

A longer amortization period will have lower monthly payments, but you will need to pay more interest overall.

Longer amortization periods tend to give the borrower increased flexibility, enabling them to pre-pay the loan if they have excess cash, rather than tying them to a payment schedule they can’t meet.

How is the amortization period calculated?

The amortization period is usually calculated using a table called a loan amortization schedule. It lays out what your monthly principal and interest payments will be over the lifespan of the loan.

You can also use an amortization calculator, found on the websites of most financial institutions, to get a rough sense of how your loan could be amortized.

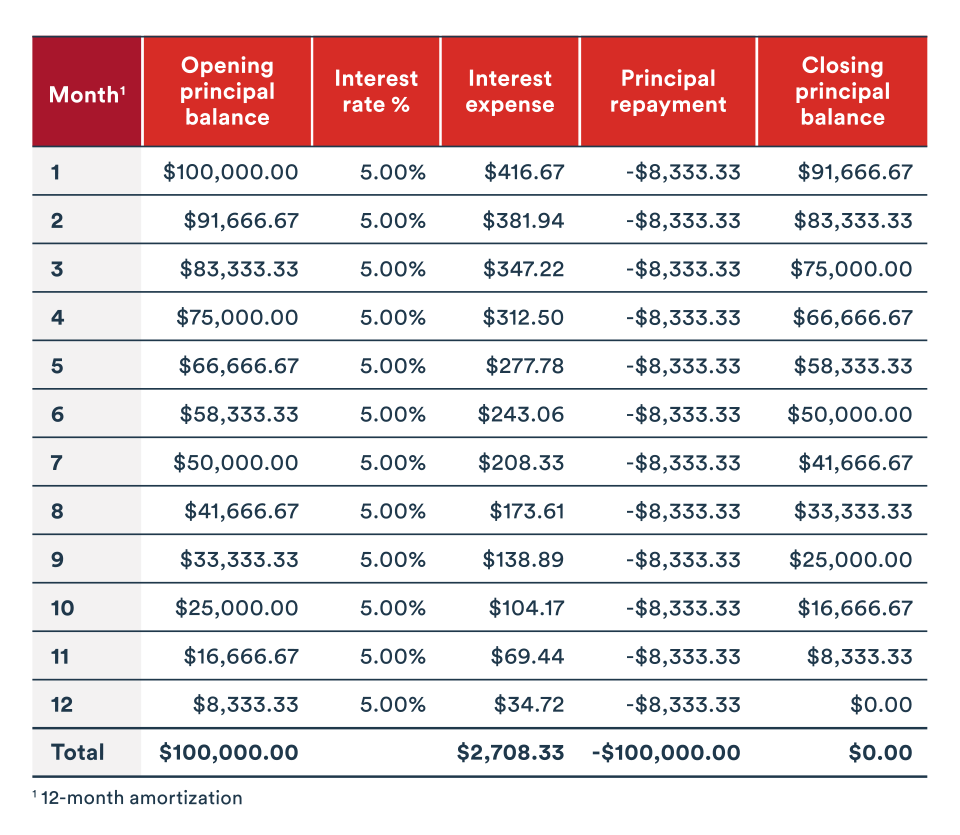

In the example below, the company has borrowed $100,000 and agreed to a 12-month amortization period at an interest rate of 5%. Monthly payments are for the principal plus interest. The table shows how the principal balance gets smaller with each payment, along with the associated interest expense.

In this amortization schedule, principal repayments remain constant over the loan term, but interest payments steadily decrease.

What is an amortization expense?

The term “amortization period” should not be confused with amortization expenses.

While both refer to financial charges over time, amortization expenses refer to the decline in value of an asset over time due to wear and tear. They are not related to the amortization period of a loan.

Next step

Use our free business loan calculator to calculate the costs of a business loan and a monthly amortization schedule.