How to manage working capital in a growing business

Even a company achieving good sales can hit a roadblock and suddenly find itself experiencing a threat to its growth.

Growth requires you to invest in inventory and, at the same time, wait for accounts receivable to be paid. This combination of factors can increase the required investment in working capital without which your sales cannot grow.

To avoid this situation, your growth projects should always include an assessment of your working capital needs. Here’s how you can complete this kind of analysis.

What is working capital?

Working capital is the amount of money your business needs to conduct its short-term operations. The working capital ratio is calculated by subtracting current liabilities from current assets.

Working capital formula

These elements fluctuate in the short term, which means they increase or decrease as business operations change. It’s this focus on the short term that distinguishes working capital from longer-term investments in capital assets, or research and development.

Current assets can generally be converted into cash over the 12 months that follow or the next operating cycle. They include:

- cash flow

- investments with a duration of up to 12 months

- accounts receivable

- inventory

Current liabilities include:

- operating line of credit

- accounts payable

- a portion of long-term debt

- accrued expenses, such as taxes payable

Let’s take the table below as an example. The company has $20,000 in current assets and $15,000 in current liabilities, and thus has $5,000 in working capital.

| Current assets | 20,000 |

| Cash flow | 5,000 |

| Accounts receivable | 5,000 |

| Inventory | 10,000 |

| Current liabilities | 15,000 |

| Operating line of credit | 12,000 |

| Accounts payable | 3,000 |

| Working capital | 5,000 |

Liquidity ratio:

Working capital can also be assessed using the current ratio (working capital ratio). It is a measure of liquidity, meaning the business’s ability to meet its payment obligations as they fall due.

This is measured by dividing total current assets by total current liabilities.

Current ratio formula

For example, let’s say a corporation has $120,000 in current assets and $70,000 in current liabilities. The current ratio will therefore be calculated as follows:

This gives the company a healthy current ratio.

Generally, the higher the ratio, the more flexibility you have to grow your business.

If the ratio decreases, you’ll need to find out why. The ideal ratio depends on the industry and particular circumstances.

If it’s less than 1:1, it usually means you are having trouble paying your bills. Moreover, you may experience difficulties even if your ratio is greater than 1:1, depending on how quickly you can sell your inventory and recover your receivables. A 2:1 ratio usually allows the company to operate comfortably.

How does money flow through your business?

The cash conversion cycle is an important concept in cash flow management.

It measures how quickly your company converts cash into inventory and then converts it back into cash.

Let’s look at an example:

- You buy materials to produce your goods. You will obviously have to pay your supplier. This debt is added to your accounts payable.

- You then make a product and keep some materials in your warehouse. These are considered inventory.

- You make a sale and deliver a product to a customer. It may take several days after you deliver the product to get paid for it. In the meantime, this customer owes you money, so this amount is added to your accounts receivable.

You can then pay your supplier with the cash generated from sales and purchase more inventory.

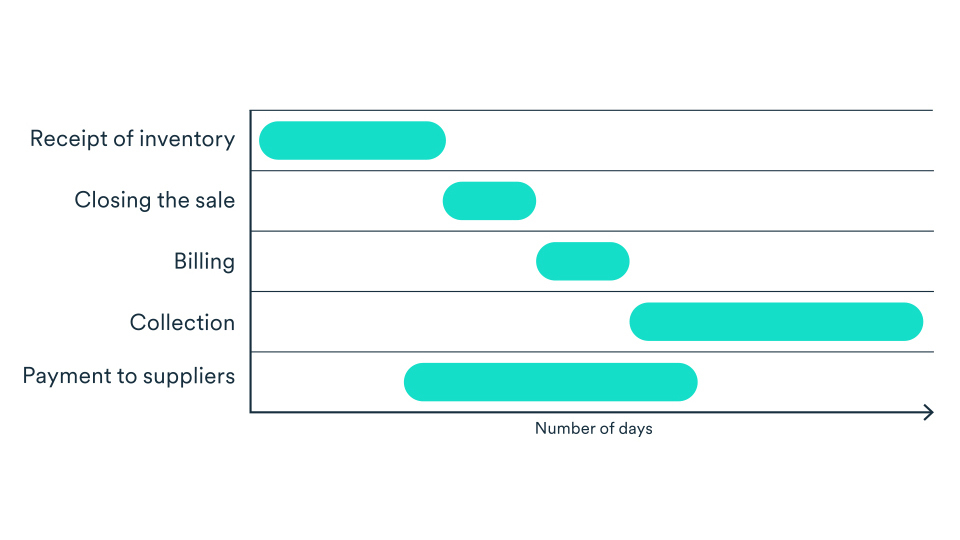

Example of a cash conversion cycle

In this example, the business has a 100-day cash conversion cycle. Let’s add up the inventory storage time and the time it takes for accounts receivable to be paid, and subtract the time it takes to pay suppliers. A hundred days to receive payment is seen by many as excessive.

If it takes too long, your funds will be locked in for a considerable period with no returns, which could make it hard for you to pay your bills.

In a perfect world, the time between the paying and receiving of accounts owed would be short enough so that the customers’ money could be used to pay suppliers. But that’s usually not the case for most businesses.

That means your business will find itself financing accounts receivable for some time until they are paid up. It’s that cash from sales that you’ll need to refill your inventory. In other words, you’ll need enough working capital to meet your company’s needs.

What happens to working capital when your business grows?

Your company’s working capital will also have to increase alongside your revenue, especially if you’re selling products. Increasing sales typically leads to additional cash requirements to purchase inventory and finance new accounts receivable.

It is therefore recommended that you anticipate the amount of money needed to support your growth.

How do you plan for the additional working capital required for your growth?

To calculate your working capital requirements, use the projected increase in your sales to estimate how much cash you will need to cover your additional outlays on inventory, accounts payable and accounts receivable.

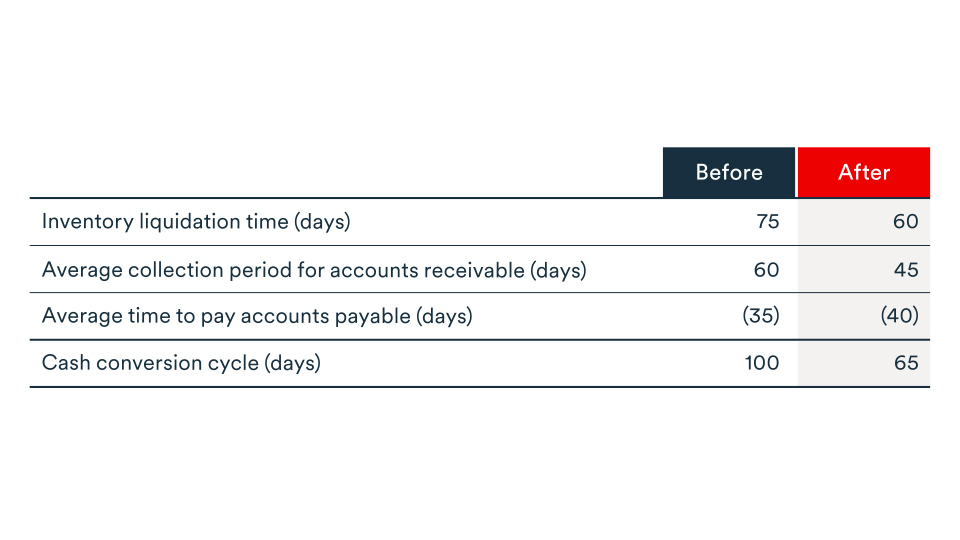

Let’s imagine that your business’s cash conversion cycle is measured as follows:

In this situation, if your sales increase by $25,000 annually, you would need $8,390 in additional working capital.

Download the working capital forecast calculator

This calculation is somewhat complex and is not done by hand. That’s why we’ve provided you with a free working capital calculator.

Get your working capital calculator. It’s 100% free.

You can use the calculator to test various sales scenarios (optimistic, pessimistic, realistic) to determine how much working capital you’ll need to support your growth.

How to increase your working capital when your business is growing

Have you estimated how much additional working capital you need to keep growing? If not, then it’s time think about how you can increase your working capital. Here are some options:

1. Optimize your operations

To improve your working capital (which is Current Assets minus Current Liabilities), you’ll need to either increase your current assets or reduce your current liabilities.

You can optimize your working capital by:

- reducing the time it takes to collect payment on your accounts receivable, such as by invoicing your customers as soon as the goods are delivered

- reducing your fixed production costs relative to your sales volume

- increasing inventory turnover, while ensuring sound inventory management

- extending the deadline to settle your accounts payable, while continuing to pay your bills on time

To predict how these optimizations will impact your working capital, you can again look to the calculator. You may, for example, want to check what effect shortening collection times will have on your accounts receivable or what an increase will do to your inventory turnover rate.

2. Use profits to fuel growth

It’s natural to reinvest your profits into your working capital. If those profits are significant enough, they alone could support your growth.

If your company pays dividends and anticipates a significant increase in sales, cutting or reducing them could free up funds.

3. Finance your growth

We don’t recommend using working capital to finance a purchase with a long repayment period, such as for a building or large piece of equipment. Aside from making your business less nimble, a move like this will, in the eyes of some financial institutions, make your financial health appear diminished and your business at greater risk. A long-term loan is a better option for fixed assets.

You can also use a working capital loan, also known as a cash flow loan, to increase your working capital when looking to finance growth projects.

Financial institutions typically provide working capital loans based on past and projected cash flows. These loans are generally amortized over a relatively short period of four to eight years.

For example, this loan could be useful when:

- you believe your profits will not be significant enough to cover your future working capital needs

- your line of credit is approaching your financial institution’s limit

- you require more leverage

4. Inject shareholders’ equity

If you don’t think you’ll have enough funds to keep growing your company, then injecting shareholders’ equity into your business could also help you stave off any loss in growth.

Generally speaking, organizations or individuals who invest money in a company, receive shares in return. However, having multiple shareholders in your company will lead to equity dilution.

If you are the sole owner of the business, run an analysis and estimate the returns. You must ensure that expected returns to your business exceed your personal losses.

Next step

Learn how forecasting sales and inventory and reducing customer payment times can improve your cash conversion cycle by downloading the free guide for entrepreneurs: Taking Control of Your Cash Flow.